【為替介入のメカニズムと確率トレンド🌟】『Modeling Sterilized Interventions and Balance Sheet Effects of Monetary Policy in a New-Keynesian Framework』:IMF Working Paper No.13

卒業論文にはこだわりました💛

私もいよいよ卒業論文の執筆に

取りかかる時期がやって参りました👍

何事もアウトプット前提の

インプットが大事であると

noteで毎日発信してきました。

これは、どのような内容で

あっても当てはまります👍

論文を一概に読んでも

記憶に残っていなかったり

大切な観点を忘れてしまっていたり

したら卒業論文の進捗は滞って

いたことでしょう…

この投稿では、収益化をすることはなく

先行研究などのコンテンツを正しく引用し

適切な発信ができるように努めます📝

私の卒論執筆への軌跡を

どうぞ最後までご愛読ください📖

今回の参考文献🔥

今回、読み進めていく論文は

こちらのURLになります👍

Author/Editor:Jaromir Benes ; Andrew Berg ; Rafael A Portillo ; David Vávra

Publication Date: January 14, 2013

前回のお復習い📝

Modeling Sterilized Interventions and Balance Sheet Effects of Monetary Policy in a New-Keynesian Framework

Author/Editor:Jaromir Benes ; Andrew Berg ; Rafael A Portillo ; David Vávra

Publication Date: January 14, 2013

V.Discussion

今回の投稿では、取り上げる先行研究の大事なところをピックアップしていくことにします

Steady state and two spreadsの箇所は割愛させていただきます💦

本文などご興味のある際は、ぜひ該当リンクからご確認ください📝

一度、ここまで登場したモデルの式を振り返ります

$$

\\Interest rate Reaction Function\\ of the Central Bank\\ \\

i^T =\bar{i}+\alpha(\pi-\pi^T)+\delta\hat{y}+\chi\Upsilon \cdots(1)\\ \\\\

\Upsilon=\eta\Delta s +(1-\eta)(s-s^T)\cdots (2)\\\therefore ρ_s = α_s = δ_s = 0 \\ \\ \\log(\frac{F}{L})=log(\frac{\bar{F}}{L})-\omega log(\frac{S^T}{S})-ϑ log(\frac{S_{-1}}{S})\cdots(3)\\ \\

i=i_t^T \cdots (4)\\ \\i^T=\rho i_{-1}^T+(1-\rho)(\bar{i}+\alpha(\pi-\pi^T)+\delta\hat{y}+\chi\Upsilon )\cdots(5)\\ \\s^T=\rho s^T_{-1}+(1-\rho)(\bar{s}-\alpha_s(\pi-\pi^T)-\delta_s\hat{y})\\ \\exp(i) = exp(i^∗) \frac{S_{+1}} {S} + Ω_O( \frac{F}{ P} ), Ω^′_ O(F/P) > 0 \cdots (6)\\ \\exp(j) = exp(i^∗) \frac{S_{+1}}{ S} + Ω_L \cdots (7) \\ = exp(i) + Ω_L − Ω_O( \frac{F}{ P} )\\ \\

P C − L = − exp(j_{−1})L_{−1} + Π − Ψ(L/P)\\ \\ Ψ^ ′ (L/P) > 0, Ψ^{′′}(L/P) > 0\cdots (8)\\ \\

\frac{λ} {λ_{+1}} (1 − ϱ (L/P)) = β exp(j) \cdots (9)\\ \\ P λ = U^ ′ (C)

$$

Intervention mechanism

The second important feature of the model is the exchange rate stabilization mechanism outside the steady state.

When the exchange rate rises above the target level (i.e. depreciates), the central bank draws on its reserves (relative to NFL) to defend the currency.

This results in falling UIP premium ΩO(F/P) in (6), which then works towards currency strengthening (ceteris paribus).19

19:In the baseline calibration, holding expectations and interest rates constant, a one percent increase in reserves—relative to its steady state value—depreciates the exchange rate by one fourth of a percent.

このモデルの2番目の重要な特徴は、定常状態からは外れた(outside the steady state)状態における為替レート安定化メカニズムに言及していることです。

為替レートが目標水準を超えて上昇(つまり円安)すると、中央銀行は通貨を守るために(NFLと比較して)外貨準備を利用しています。

この結果、(6)式でUIP プレミアムΩ_O(F/P) が低下し、通貨高に向かうこと(ceteris paribus)になります(注19)

注19:期待と金利を一定に保ったベースライン調整では、定常状態の価値と比較して外貨準備が1パーセント増加すると、為替レートは、4分の1パーセント下落します。

One attractive feature of this intervention mechanism is that it can help control the behavior of the exchange rate, without affecting the stochastic behavior of the policy rate.

In particular, it can be calibrated so that the exchange rate fluctuates within a pre-specified probabilistic corridor (given the variance of the model’s structural shocks).

For instance, for ω large, the exchange rate will be fixed at its target level S^T.

This is suitable for modeling hard and crawling pegs.

For ω approaching zero, the exchange rate will be fully flexible, as the central bank refrains from intervening against exchange rate deviations.

The intermediate cases provide for modeling of ’soft’ exchange rate corridors, i.e., corridors without enforceable hard boundaries.

On the other hand, parameter ϑ introduces “leaning–against–the–wind” interventions that we will use to model a managed float.

この介入メカニズムの魅力的な特徴の1つは、政策金利の確率的挙動(the stochastic behavior of the policy rate)に影響を与えることなく、為替レートの挙動を制御できることです。

特に、(モデルの構造的衝撃の分散を考慮すると)為替レートが事前に指定された確率的コリドー内で変動するように調整できる点にあります。

たとえば、ωが大きい場合、為替レートはその目標レベル$${S^T}$$に固定されます。

これは、硬くて這うペグ(hard and crawling pegs)のモデル化に適しています。

ωがゼロに近づくと、中央銀行が為替レートの逸脱に対して介入を控えるため、為替レートは完全に柔軟になります。

中間のケースでは「ソフト」為替レートコリドー(回廊)、つまり強制的なハード境界のないコリドー(回廊)のモデル化が提供されます。

一方、パラメーター ϑは、管理フロートのモデル化に使用する「風に逆らう介入:“leaning–against–the–wind” interventions」を導入します。

21頁まで先行研究の内容を割愛します…

Limits of interventions

Our analysis suggests that interventions are a viable policy instrument that could be used in a systematic way to improve monetary policy performance.

However, two broad sets of arguments qualify that conclusion.

私たちの分析によれば、介入は実行可能な政策手段(viable policy instrument)であり、金融政策のパフォーマンスを改善する体系的な方法です。

ただし、大きく分けて2つのセットからなる議論は、その結論を修飾するものです。

First, our analysis abstracts from practical consequences of markets knowing the central bank’s intervention reaction function.

Market knowledge of such a function for interest rates is commonly assumed and often desirable, but intervention and exchange rate rules are more problematic.

Suck an awareness by the markets may help the central bank to achieve its objectives more easily, but it could also lead to lethal speculative attacks.

As a result, most intervening central banks prefer to keep their intervention tactics (i.e. the reaction function) hidden, if possible, to preserve credibility.

第一に、私たちの分析は、中央銀行の介入反応関数(the central bank’s intervention reaction function)を知っている市場の実際的な結果を抽象化しています。

金利に関するこのような関数に関する市場の知識は一般的に想定されており、多くの場合望ましいものですが、介入と為替レートのルールにはさらに問題があります。

市場の意識を奪うことは、中央銀行がその目的をより容易に達成するのに役立つかもしれないが、致命的な投機的攻撃につながる可能性もあります。

その結果、介入するほとんどの中央銀行は、信頼性を維持する(preserve credibility)ために、可能であれば介入戦術(intervention tactics)、つまり、反応機能を隠しておくことが好ましいとされるのです。

The threat of an attack arises especially when the markets believe that the central bank does not understand the nature of the exchange rate movements.

While our analysis assumes the central bank always knows perfectly what kind of shock it deals with, in reality this perfect knowledge is difficult to achieve and markets often have a different opinion, leading them to probe the central bank’s resolve.

攻撃の脅威(The threat of an attack)は、中央銀行が為替レートの変動の性質を理解していないと市場が信じている場合に特に生じます。

私たちの分析では、中央銀行がどのような種類のショックに対処しているかを常に完全に知っていると想定しています。

しかしながら、実際には、この完璧な知識を得るのは難しく、市場はしばしば異なる意見を持ち、中央銀行の政策決定を探ることにつながります、

A typical example is when markets and central banks disagree whether the exchange rate movement is driven by permanent or temporary shocks.

Permanent shocks, i.e. shocks changing the steady state level of real variables, require a different response than temporary shocks.

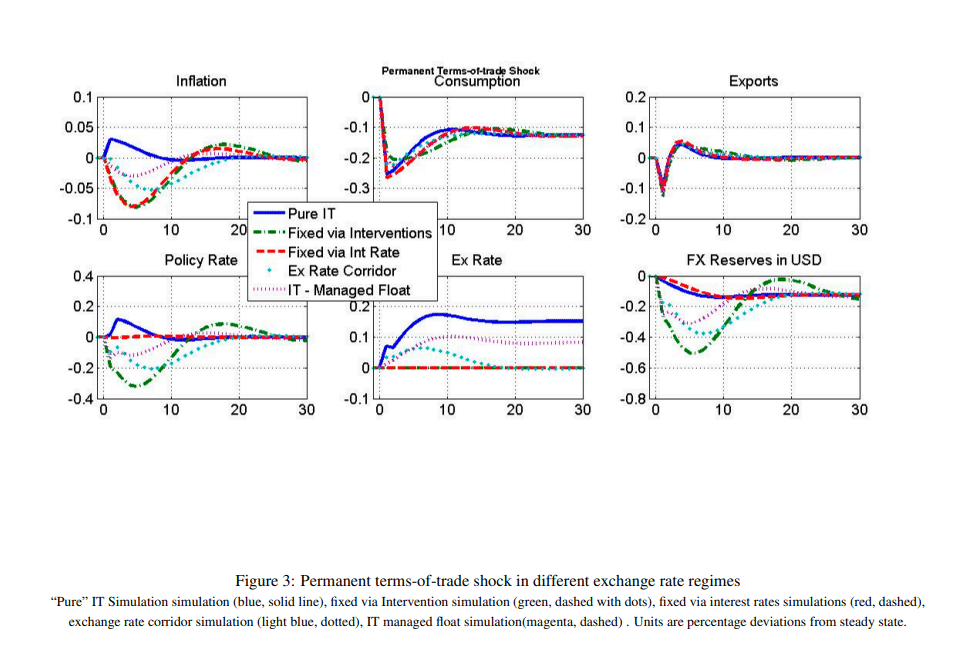

Figures 2 and 3 show model reactions to temporary and permanent terms-of-trade shocks.

The initial size of the shock is same in both cases, but while the shock gradually dissipates in Figure 2, the terms-of-trade remain at a permanently lower level in Figure 3.

典型的な例は、市場が次のような場合です。

そして中央銀行は、為替レートの変動が永続的なショックによって引き起こされるのか、それとも一時的なショックによって引き起こされるのかについて意見が一致していないときが該当します。

永続的なショック(Permanent shocks)、つまり実変数の定常状態レベルを変化させるショックには、一時的なショックとは異なる応答が必要です。

図2と図3は、一時的および永続的な交易条件ショックに対するモデル反応を示しています。

あどちらの場合もショックの初期の大きさは同じですが、図2ではショックが徐々に消えていく一方で、図3では交易条件が恒久的に低いレベルに留まります。

The permanently worse terms-of-trade require permanent real adjustments, such as a permanently weaker real exchange rate (not shown) and a permanently lower consumption level.

The new weaker real exchange rate level can be achieved either via a weaker nominal exchange rate or a permanently lower price level.

The former is the outcome under the floating regimes, while fixed exchange rate regimes tend to experience deflation.

At the same time the fixed regimes kept by interventions require a larger spending of reserves to keep the exchange rate at the parity.

交易条件が永続的に悪化すると、実質為替レートの永続的な低下(図示せず)や消費水準の永続的な低下など、永続的な実質調整が必要になります。

新たな実質為替レートの下落水準は、名目為替レートの下落または恒久的な低価格水準のいずれかによって達成できます。

前者は変動相場制(the floating regimes)の下での結果ですが、固定為替相場制(fixed exchange rate regimes)ではデフレが発生する傾向があります。

同時に、介入によって維持される固定体制では、為替レートを平価に維持するために外貨準備のより多くの支出が必要となります。

本日の解説は、ここまでとします。

このような歴史や先行研究をしっかりと

理解した上で、卒業論文執筆に

取り組んでいったことが

「優秀論文」に選出されたことに

繋がったのではないでしょうか?

読み終えた先行研究📚

『日本の為替介入の分析』 伊藤隆敏・著

経済研究 Vol.54 No.2 Apr. 2003

『Effects of the Bank of Japan’s intervention on yen/dollar exchange rate volatility』21 November 2004

Toshiaki Watanabe (a), Kimie Harada (b)

『The Effects of Japanese Foreign Exchange Intervention: GARCH Estimation and Change Point Detection』

Eric Hillebrand Gunther Schnabl Discussion

Paper No.6 October 2003

私の研究テーマについて🔖

私は「為替介入の実証分析」をテーマに

卒業論文を執筆しようと考えています📝

日本経済を考えたときに、為替レートによって

貿易取引や経常収支が変化したり

株や証券、債権といった金融資産の収益率が

変化したりと日本経済と為替レートとは

切っても切れない縁があるのです💝

(円💴だけに・・・)

経済ショックによって

為替レートが変化すると

その影響は私たちの生活に大きく影響します

だからこそ、為替レートの安定性を

担保するような為替介入はマクロ経済政策に

おいても非常に重要な意義を持っていると

推測しています

決して学部生が楽して執筆できる

簡単なテーマを選択しているわけでは無いと信じています

ただ、この卒業論文をやり切ることが

私の学生生活の集大成となることは事実なので

最後までコツコツと取り組んで参ります🔥

本日の解説は、以上とします📝

今後も経済学理論集ならびに

社会課題に対する経済学的視点による説明など

有意義な内容を発信できるように

努めてまいりますので

今後とも宜しくお願いします🥺

マガジンのご紹介🔔

こちらのマガジンにて

卒業論文執筆への軌跡

エッセンシャル経済学理論集、ならびに

【国際経済学🌏】の基礎理論をまとめています

今後、さらにコンテンツを拡充できるように努めて参りますので何卒よろしくお願い申し上げます📚

最後までご愛読いただき誠に有難うございました!

あくまで、私の見解や思ったことを

まとめさせていただいてますが

その点に関しまして、ご了承ください🙏

この投稿をみてくださった方が

ほんの小さな事でも学びがあった!

考え方の引き出しが増えた!

読書から学べることが多い!

などなど、プラスの収穫があったのであれば

大変嬉しく思いますし、投稿作成の冥利に尽きます!!

お気軽にコメント、いいね「スキ」💖

そして、お差し支えなければ

フォロー&シェアをお願いしたいです👍

今後とも何卒よろしくお願いいたします!