[FAR] Lease Accounting について ③

さて今回は Lessor の視点から Lease Accounting を見ていこうと思います。

Lessee ではなく Lessor の視点になるので注意してください。

ではいきましょう。

よろしくお願いします。

そもそも Sales-type Lease とは?

Sales type lease とは、貸し手が借り手に対して実際に製品を販売していると仮定し、販売損益を認識する方法のことです。

ではどのように Journal Entry を行うのでしょうか?(これが一番大事. 他の方法とどう違うのか)

前回と同じ例題を使ってみていきましょう。

Your company leases a machine for 3 years.

The machine is expected to have a residual value of $15,000 at the end of the lease. Your company will receive a lease payment of $20,000 at the beginning of each year. The lessor's implicit interest rate is 6%.

ここで、

PV of residual Value = $12,594

PV of lease payment = $56,668

Fair Value of Machine = $69,262 = $12,594 + $56,668

*今回 Lessor 側なので、 lease payment を receive します。

ここであれ?と思われたかもしれません

2024年分はいったい何なのかという点です。

これは、帰ってきた Machine の資産を表しています。なので、いったん Payment Receivedとしてカウントします。

この場合の Journal Entryって?

さて、以上の例文をベースに Journal Entry を組み立て行きましょう。

今回、基本利益を得る側なので、Lease Receivable (AR的な奴)が多く登場します。

一番最初は、これくらい得るだろうと予測した分を書いていきます。

まず大前提として Finance Lease の場合、Leaseしたものは資産の販売 / 転売 として認識されます。よって会社 A から Bへと資産の所有権が移ったと考え、会社A は自社の Inventoryが減り、それと同様に 売り上げ(販売)があったと考え,販売にかかったであろう COGS も同様に増えるのです。(また、会計の原則により、売上を記録する際にはその売上に直接関連するコストも記録する必要があります。)

The 1st Payment

The 2nd Payment

The 3rd Paymeあげ

最後に、Machine が返ってくるので、それを計上していきます。

Lessor 視点の Operating Lease

さて前回と同様に例題を使って見ていきましょう。

E.g.

Your company leases a machine for 3 years to ABC company. Your company will make a lease payment of $20,000 at the beginning of each year.

The machine is expected to have a useful economic life of 10 years, and your company uses a straight-line method for depreciation.

The cost basis for the machine is $50,000.

The expected salvage value of the machine is zero.

さて、この場合どのように Journal Entry を入れていけばいいのでしょうか?

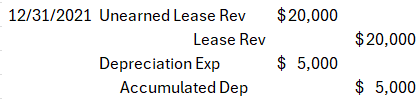

最初の年は、Unearned Rev として認識します。まだ、きちんと Rev として認識していないためです。

End of the year (The 1st Payment)

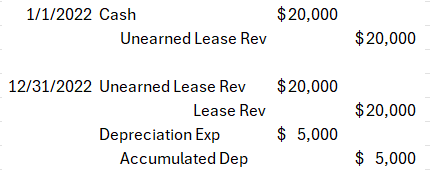

The 2nd Year (次の年の初めと終わりも同様になります。)

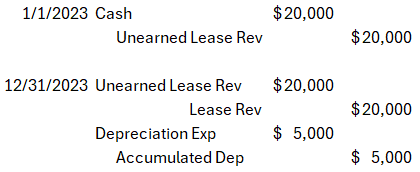

The 3rd year

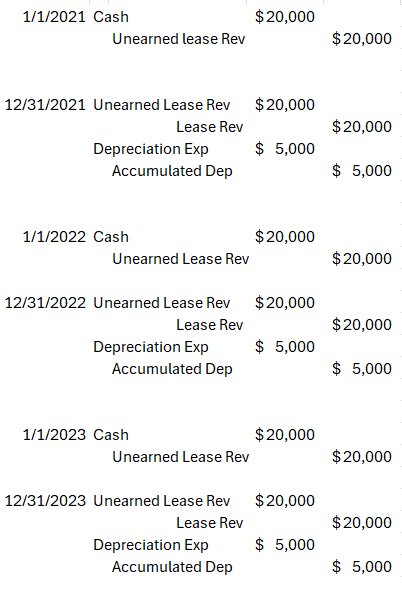

まとめると

このような Journal Entry になると思います。

最後にJournal Entry を見比べてみて…

以下がまとめの表です。

一度自分で Journal Account や T-Account を作成し見比べてみるのもありかもしれません。

今回は以上です。

次回は Direct Fiance Lease といった、引き続き Lessor 側の Account を見ていきたいと思います。

お疲れさまでした。