第7章 線形モデル編: 第5節 線形回帰で株価予測をする

はじめに

本記事では、線形回帰モデルとリッジ回帰とラッソ回帰から交差検定を用いて予測モデルを作成します。予測モデルの結果を評価し、最後に3つのモデルを比較したいと思います。

リッジ回帰とラッソ回帰についてはこちらの記事が分かりやすいです。

インポートと設定

import warnings

warnings.filterwarnings('ignore')%matplotlib inline

from time import time

from pathlib import Path

import pandas as pd

import numpy as np

from scipy.stats import spearmanr

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression, Ridge, Lasso

from sklearn.pipeline import Pipeline

import seaborn as sns

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormattersns.set_style('darkgrid')

idx = pd.IndexSliceYEAR = 252データの読み込み

with pd.HDFStore('data.h5') as store:

data = (store['model_data']

.dropna()

.drop(['open', 'close', 'low', 'high'], axis=1))data.index.names = ['symbol', 'date']data = data.drop([c for c in data.columns if 'lag' in c], axis=1)フィルタリング

data = data[data.dollar_vol_rank<100]目的変数と説明変数の定義

y = data.filter(like='target')

X = data.drop(y.columns, axis=1)

X = X.drop(['dollar_vol', 'dollar_vol_rank', 'volume', 'consumer_durables'], axis=1)ここまでは前回と同じですので、そちらも参考にしてくださいませ。

カスタムマルチ時系列交差検定

こちらのカスタムマルチ時系列交差検定について解説します。

例えば、2週間訓練して2週間テストして、それを2週間ずつズラしたいと思います。いわゆるウォークフォワード法っていう手法になります。しかも、こちらの良い所は、テスト期間の初めはデータが漏れる可能性があり(フォワードリターンの期間によって)、それでデータを一部取り除く作業もしております。

class MultipleTimeSeriesCV:

"""Generates tuples of train_idx, test_idx pairs

Assumes the MultiIndex contains levels 'symbol' and 'date'

purges overlapping outcomes"""

def __init__(self,

n_splits=3,

train_period_length=126,

test_period_length=21,

lookahead=None,

shuffle=False):

self.n_splits = n_splits

self.lookahead = lookahead

self.test_length = test_period_length

self.train_length = train_period_length

self.shuffle = shuffle

def split(self, X, y=None, groups=None):

unique_dates = X.index.get_level_values('date').unique()

days = sorted(unique_dates, reverse=True)

split_idx = []

for i in range(self.n_splits):

test_end_idx = i * self.test_length

test_start_idx = test_end_idx + self.test_length

train_end_idx = test_start_idx + + self.lookahead - 1

train_start_idx = train_end_idx + self.train_length + self.lookahead - 1

split_idx.append([train_start_idx, train_end_idx,

test_start_idx, test_end_idx])

dates = X.reset_index()[['date']]

for train_start, train_end, test_start, test_end in split_idx:

train_idx = dates[(dates.date > days[train_start])

& (dates.date <= days[train_end])].index

test_idx = dates[(dates.date > days[test_start])

& (dates.date <= days[test_end])].index

if self.shuffle:

np.random.shuffle(list(train_idx))

yield train_idx, test_idx

def get_n_splits(self, X, y, groups=None):

return self.n_splits出力例

train_period_length = 63

test_period_length = 10

n_splits = int(3 * YEAR/test_period_length)

lookahead =1

cv = MultipleTimeSeriesCV(n_splits=n_splits,

test_period_length=test_period_length,

lookahead=lookahead,

train_period_length=train_period_length)i = 0

for train_idx, test_idx in cv.split(X=data):

train = data.iloc[train_idx]

train_dates = train.index.get_level_values('date')

test = data.iloc[test_idx]

test_dates = test.index.get_level_values('date')

df = train.reset_index().append(test.reset_index())

n = len(df)

assert n== len(df.drop_duplicates())

print(train.groupby(level='symbol').size().value_counts().index[0],

train_dates.min().date(), train_dates.max().date(),

test.groupby(level='symbol').size().value_counts().index[0],

test_dates.min().date(), test_dates.max().date())

i += 1

if i == 10:

break

'''

63 2017-08-16 2017-11-14 10 2017-11-15 2017-11-29

63 2017-08-02 2017-10-30 10 2017-10-31 2017-11-14

63 2017-07-19 2017-10-16 10 2017-10-17 2017-10-30

63 2017-07-05 2017-10-02 10 2017-10-03 2017-10-16

63 2017-06-20 2017-09-18 10 2017-09-19 2017-10-02

63 2017-06-06 2017-09-01 10 2017-09-05 2017-09-18

63 2017-05-22 2017-08-18 10 2017-08-21 2017-09-01

63 2017-05-08 2017-08-04 10 2017-08-07 2017-08-18

63 2017-04-24 2017-07-21 10 2017-07-24 2017-08-04

62 2017-04-10 2017-07-07 10 2017-07-10 2017-07-21

'''視覚化ツール

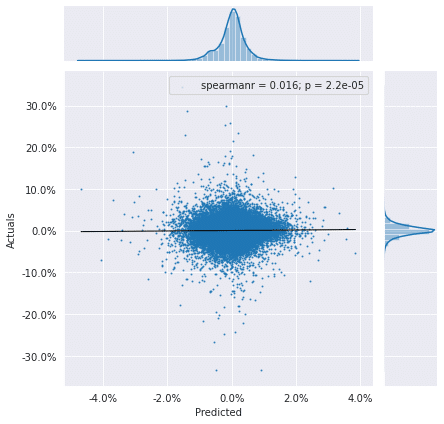

予測値と実際の値の散布図

def plot_preds_scatter(df, ticker=None):

if ticker is not None:

idx = pd.IndexSlice

df = df.loc[idx[ticker, :], :]

j = sns.jointplot(x='predicted', y='actuals',

robust=True, ci=None,

line_kws={'lw': 1, 'color': 'k'},

scatter_kws={'s': 1},

data=df,

stat_func=spearmanr,

kind='reg')

j.ax_joint.yaxis.set_major_formatter(

FuncFormatter(lambda y, _: '{:.1%}'.format(y)))

j.ax_joint.xaxis.set_major_formatter(

FuncFormatter(lambda x, _: '{:.1%}'.format(x)))

j.ax_joint.set_xlabel('Predicted')

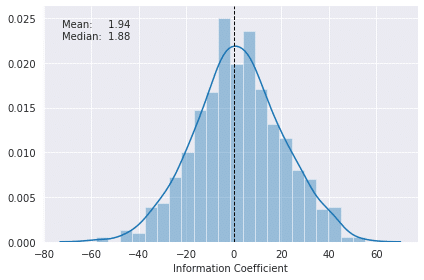

j.ax_joint.set_ylabel('Actuals')日次情報係数(IC)分布

情報係数定義:

情報係数とは、リターンと投資指標の相関係数です。

def plot_ic_distribution(df, ax=None):

if ax is not None:

sns.distplot(df.ic, ax=ax)

else:

ax = sns.distplot(df.ic)

mean, median = df.ic.mean(), df.ic.median()

ax.axvline(0, lw=1, ls='--', c='k')

ax.text(x=.05, y=.9,

s=f'Mean: {mean:8.2f}\nMedian: {median:5.2f}',

horizontalalignment='left',

verticalalignment='center',

transform=ax.transAxes)

ax.set_xlabel('Information Coefficient')

sns.despine()

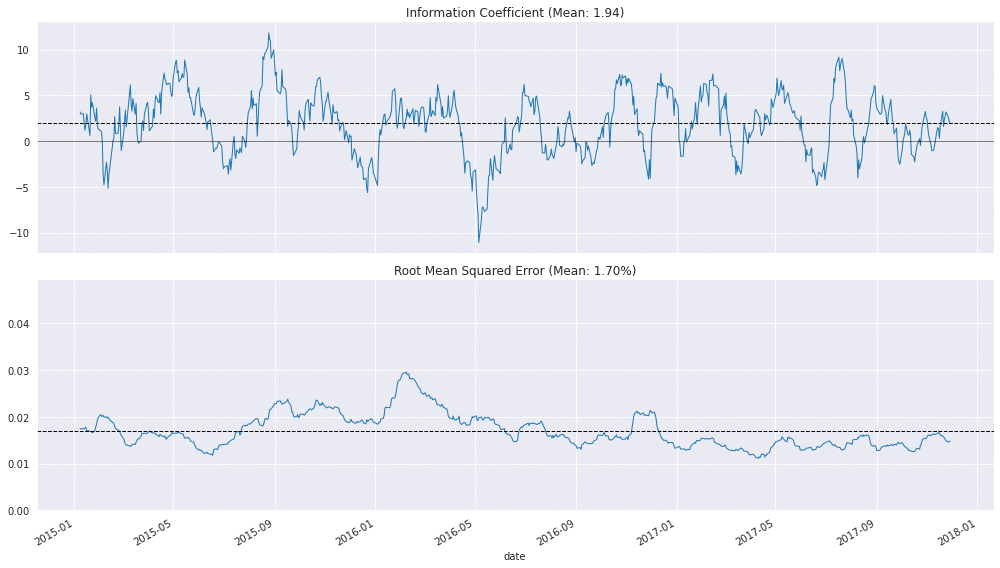

plt.tight_layout()ローリング日次IC

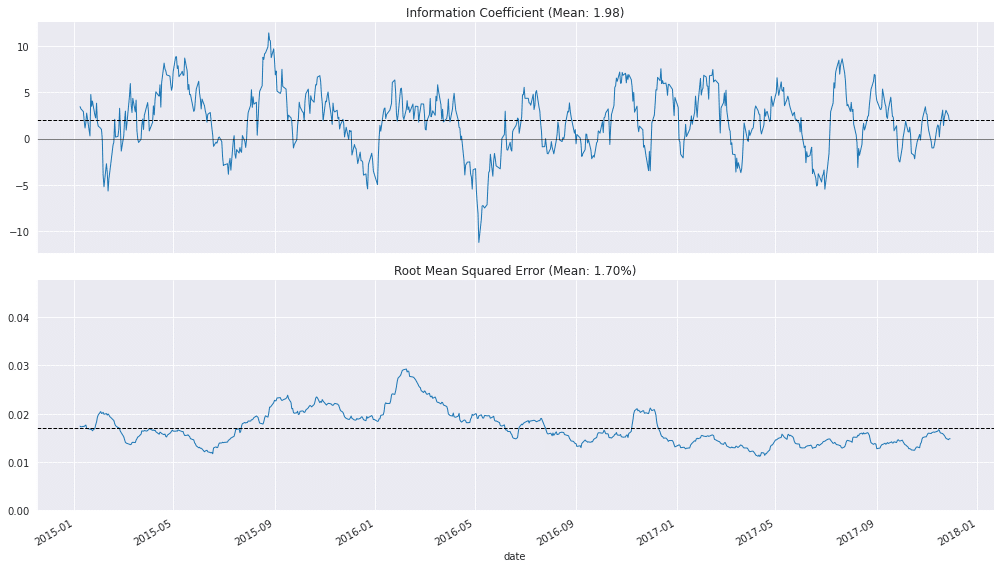

def plot_rolling_ic(df):

fig, axes = plt.subplots(nrows=2, sharex=True, figsize=(14, 8))

rolling_result = df.sort_index().rolling(21).mean().dropna()

mean_ic = df.ic.mean()

rolling_result.ic.plot(ax=axes[0],

title=f'Information Coefficient (Mean: {mean_ic:.2f})',

lw=1)

axes[0].axhline(0, lw=.5, ls='-', color='k')

axes[0].axhline(mean_ic, lw=1, ls='--', color='k')

mean_rmse = df.rmse.mean()

rolling_result.rmse.plot(ax=axes[1],

title=f'Root Mean Squared Error (Mean: {mean_rmse:.2%})',

lw=1,

ylim=(0, df.rmse.max()))

axes[1].axhline(df.rmse.mean(), lw=1, ls='--', color='k')

sns.despine()

plt.tight_layout()sklearnによる線形回帰

交差検定セットアップ

train_period_length = 63

test_period_length = 10

n_splits = int(3 * YEAR / test_period_length)

lookahead = 1

cv = MultipleTimeSeriesCV(n_splits=n_splits,

test_period_length=test_period_length,

lookahead=lookahead,

train_period_length=train_period_length)線形回帰モデルで交差検定する

%%time

target = f'target_{lookahead}d'

lr_predictions, lr_scores = [], []

lr = LinearRegression()

for i, (train_idx, test_idx) in enumerate(cv.split(X), 1):

X_train, y_train, = X.iloc[train_idx], y[target].iloc[train_idx]

X_test, y_test = X.iloc[test_idx], y[target].iloc[test_idx]

lr.fit(X=X_train, y=y_train)

y_pred = lr.predict(X_test)

preds = y_test.to_frame('actuals').assign(predicted=y_pred)

preds_by_day = preds.groupby(level='date')

scores = pd.concat([preds_by_day.apply(lambda x: spearmanr(x.predicted,

x.actuals)[0] * 100)

.to_frame('ic'),

preds_by_day.apply(lambda x: np.sqrt(mean_squared_error(y_pred=x.predicted,

y_true=x.actuals)))

.to_frame('rmse')], axis=1)

lr_scores.append(scores)

lr_predictions.append(preds)

lr_scores = pd.concat(lr_scores)

lr_predictions = pd.concat(lr_predictions)

'''

CPU times: user 10.6 s, sys: 885 ms, total: 11.5 s

Wall time: 2.94 s

'''結果の保持

lr_scores.to_hdf('data.h5', 'lr/scores')

lr_predictions.to_hdf('data.h5', 'lr/predictions')lr_scores = pd.read_hdf('data.h5', 'lr/scores')

lr_predictions = pd.read_hdf('data.h5', 'lr/predictions')評価結果

lr_r, lr_p = spearmanr(lr_predictions.actuals, lr_predictions.predicted)

print(f'Information Coefficient (overall): {lr_r:.3%} (p-value: {lr_p:.4%})')

'''

Information Coefficient (overall): 1.559% (p-value: 0.0022%)

'''予測 vs 観測 散布図

plot_preds_scatter(lr_predictions)

日次IC分布

plot_ic_distribution(lr_scores)

ローリング日次IC

plot_rolling_ic(lr_scores)

リッジ回帰

ridge_alphas = np.logspace(-4, 4, 9)

ridge_alphas = sorted(list(ridge_alphas) + list(ridge_alphas * 5))n_splits = int(3 * YEAR/test_period_length)

train_period_length = 63

test_period_length = 10

lookahead = 1

cv = MultipleTimeSeriesCV(n_splits=n_splits,

test_period_length=test_period_length,

lookahead=lookahead,

train_period_length=train_period_length)交差検定を走らせる

target = f'target_{lookahead}d'

X = X.drop([c for c in X.columns if 'year' in c], axis=1)%%time

ridge_coeffs, ridge_scores, ridge_predictions = {}, [], []

for alpha in ridge_alphas:

print(alpha, end=' ', flush=True)

start = time()

model = Ridge(alpha=alpha,

fit_intercept=False,

random_state=42)

pipe = Pipeline([

('scaler', StandardScaler()),

('model', model)])

coeffs = []

for i, (train_idx, test_idx) in enumerate(cv.split(X), 1):

X_train, y_train, = X.iloc[train_idx], y[target].iloc[train_idx]

X_test, y_test = X.iloc[test_idx], y[target].iloc[test_idx]

pipe.fit(X=X_train, y=y_train)

y_pred = pipe.predict(X_test)

preds = y_test.to_frame('actuals').assign(predicted=y_pred)

preds_by_day = preds.groupby(level='date')

scores = pd.concat([preds_by_day.apply(lambda x: spearmanr(x.predicted,

x.actuals)[0] * 100)

.to_frame('ic'),

preds_by_day.apply(lambda x: np.sqrt(mean_squared_error(y_pred=x.predicted,

y_true=x.actuals)))

.to_frame('rmse')], axis=1)

ridge_scores.append(scores.assign(alpha=alpha))

ridge_predictions.append(preds.assign(alpha=alpha))

coeffs.append(pipe.named_steps['model'].coef_)

ridge_coeffs[alpha] = np.mean(coeffs, axis=0)

print('\n')

'''

0.0001 0.0005 0.001 0.005 0.01 0.05 0.1 0.5 1.0 5.0 10.0 50.0 100.0 500.0 1000.0 5000.0 10000.0 50000.0

CPU times: user 3min 32s, sys: 16.7 s, total: 3min 48s

Wall time: 57.7 s

'''結果の保持

ridge_scores = pd.concat(ridge_scores)

ridge_scores.to_hdf('data.h5', 'ridge/scores')

ridge_coeffs = pd.DataFrame(ridge_coeffs, index=X.columns).T

ridge_coeffs.to_hdf('data.h5', 'ridge/coeffs')

ridge_predictions = pd.concat(ridge_predictions)

ridge_predictions.to_hdf('data.h5', 'ridge/predictions')ridge_scores = pd.read_hdf('data.h5', 'ridge/scores')

ridge_coeffs = pd.read_hdf('data.h5', 'ridge/coeffs')

ridge_predictions = pd.read_hdf('data.h5', 'ridge/predictions')結果の評価

ridge_r, ridge_p = spearmanr(ridge_predictions.actuals, ridge_predictions.predicted)

print(f'Information Coefficient (overall): {ridge_r:.3%} (p-value: {ridge_p:.4%})')

'''

Information Coefficient (overall): 1.583% (p-value: 0.0000%)

'''

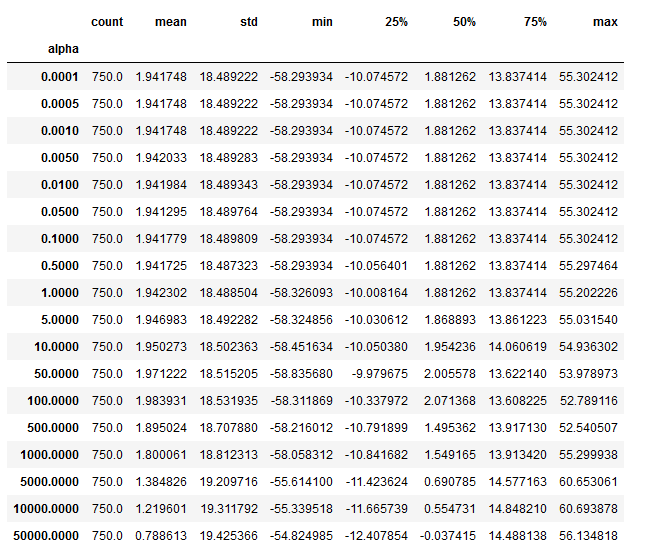

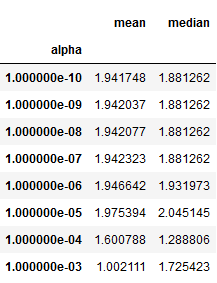

ridge_scores.groupby('alpha').ic.describe()

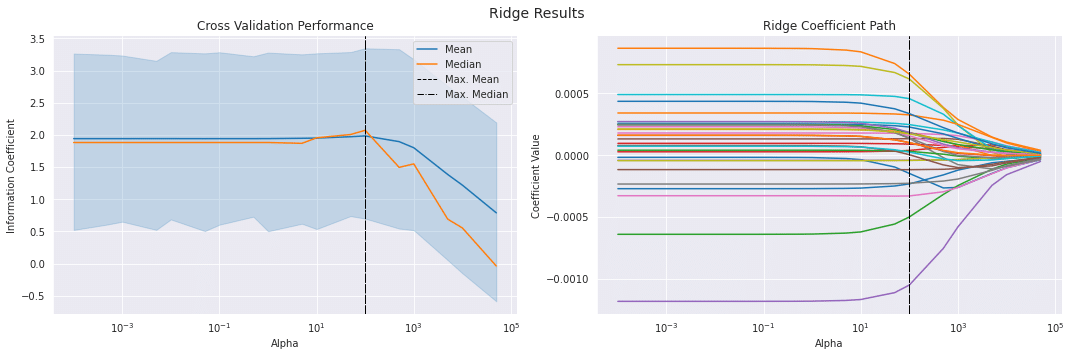

fig, axes = plt.subplots(ncols=2, sharex=True, figsize=(15, 5))

scores_by_alpha = ridge_scores.groupby('alpha').ic.agg(['mean', 'median'])

best_alpha_mean = scores_by_alpha['mean'].idxmax()

best_alpha_median = scores_by_alpha['median'].idxmax()

ax = sns.lineplot(x='alpha',

y='ic',

data=ridge_scores,

estimator=np.mean,

label='Mean',

ax=axes[0])

scores_by_alpha['median'].plot(logx=True,

ax=axes[0],

label='Median')

axes[0].axvline(best_alpha_mean,

ls='--',

c='k',

lw=1,

label='Max. Mean')

axes[0].axvline(best_alpha_median,

ls='-.',

c='k',

lw=1,

label='Max. Median')

axes[0].legend()

axes[0].set_xscale('log')

axes[0].set_xlabel('Alpha')

axes[0].set_ylabel('Information Coefficient')

axes[0].set_title('Cross Validation Performance')

ridge_coeffs.plot(logx=True,

legend=False,

ax=axes[1],

title='Ridge Coefficient Path')

axes[1].axvline(best_alpha_mean,

ls='--',

c='k',

lw=1,

label='Max. Mean')

axes[1].axvline(best_alpha_median,

ls='-.',

c='k',

lw=1,

label='Max. Median')

axes[1].set_xlabel('Alpha')

axes[1].set_ylabel('Coefficient Value')

fig.suptitle('Ridge Results', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9)

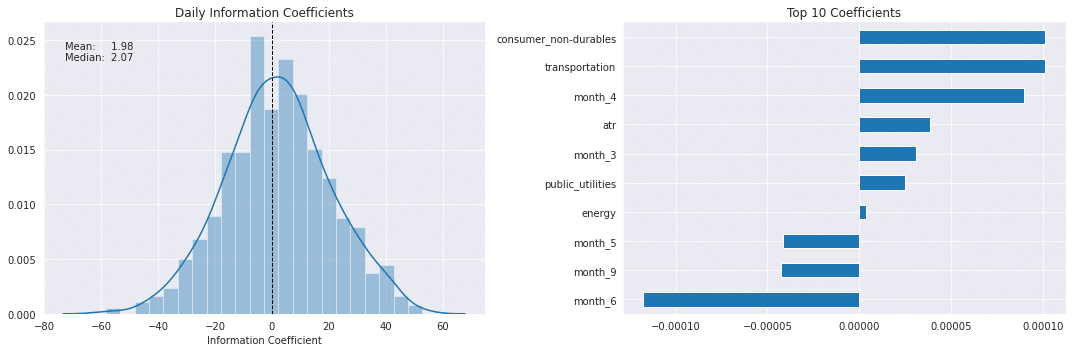

best_alpha = ridge_scores.groupby('alpha').ic.mean().idxmax()

fig, axes = plt.subplots(ncols=2, figsize=(15, 5))

plot_ic_distribution(ridge_scores[ridge_scores.alpha == best_alpha],

ax=axes[0])

axes[0].set_title('Daily Information Coefficients')

top_coeffs = ridge_coeffs.loc[best_alpha].abs().sort_values().head(10).index

top_coeffs.tolist()

ridge_coeffs.loc[best_alpha, top_coeffs].sort_values().plot.barh(ax=axes[1],

title='Top 10 Coefficients')

sns.despine()

fig.tight_layout()

plot_rolling_ic(ridge_scores[ridge_scores.alpha==best_alpha])

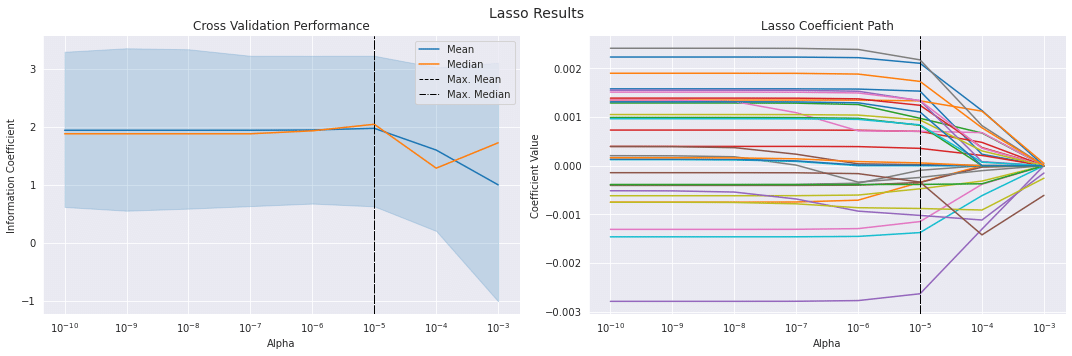

ラッソ交差検定(Lasso CV)

lasso_alphas = np.logspace(-10, -3, 8)train_period_length = 63

test_period_length = 10

YEAR = 252

n_splits = int(3 * YEAR / test_period_length) # three years

lookahead = 1cv = MultipleTimeSeriesCV(n_splits=n_splits,

test_period_length=test_period_length,

lookahead=lookahead,

train_period_length=train_period_length)交差検定する

target = f'target_{lookahead}d'

scaler = StandardScaler()

X = X.drop([c for c in X.columns if 'year' in c], axis=1)%%time

lasso_coeffs, lasso_scores, lasso_predictions = {}, [], []

for alpha in lasso_alphas:

print(alpha, end=' ', flush=True)

model = Lasso(alpha=alpha,

fit_intercept=False, # StandardScaler centers data

random_state=42,

tol=1e-3,

max_iter=1000,

warm_start=True,

selection='random')

pipe = Pipeline([

('scaler', StandardScaler()),

('model', model)])

coeffs = []

for i, (train_idx, test_idx) in enumerate(cv.split(X), 1):

t = time()

X_train, y_train, = X.iloc[train_idx], y[target].iloc[train_idx]

X_test, y_test = X.iloc[test_idx], y[target].iloc[test_idx]

pipe.fit(X=X_train, y=y_train)

y_pred = pipe.predict(X_test)

preds = y_test.to_frame('actuals').assign(predicted=y_pred)

preds_by_day = preds.groupby(level='date')

scores = pd.concat([preds_by_day.apply(lambda x: spearmanr(x.predicted,

x.actuals)[0] * 100)

.to_frame('ic'),

preds_by_day.apply(lambda x: np.sqrt(mean_squared_error(y_pred=x.predicted,

y_true=x.actuals)))

.to_frame('rmse')],

axis=1)

lasso_scores.append(scores.assign(alpha=alpha))

lasso_predictions.append(preds.assign(alpha=alpha))

coeffs.append(pipe.named_steps['model'].coef_)

lasso_coeffs[alpha] = np.mean(coeffs, axis=0)

'''

1e-10 1e-09 1e-08 1e-07 1e-06 1e-05 0.0001 0.001 CPU times: user 3min 11s, sys: 14.3 s, total: 3min 25s

Wall time: 52.1 s

'''結果の保持

lasso_scores = pd.concat(lasso_scores)

lasso_scores.to_hdf('data.h5', 'lasso/scores')

lasso_coeffs = pd.DataFrame(lasso_coeffs, index=X.columns).T

lasso_coeffs.to_hdf('data.h5', 'lasso/coeffs')

lasso_predictions = pd.concat(lasso_predictions)

lasso_predictions.to_hdf('data.h5', 'lasso/predictions')結果の評価

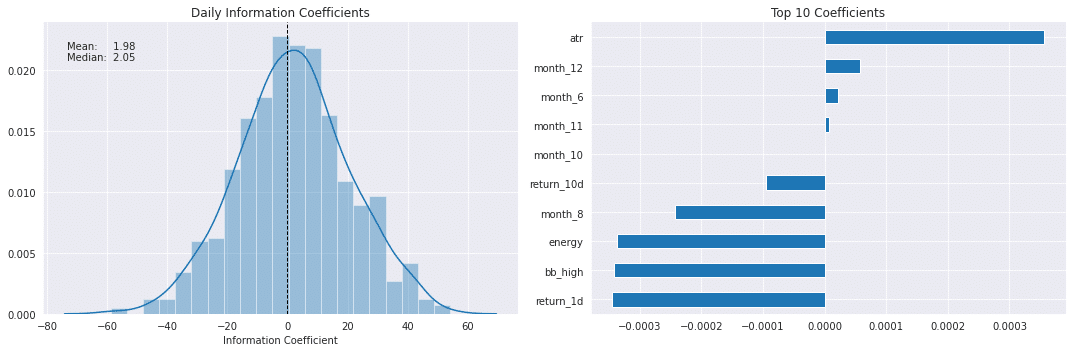

best_alpha = lasso_scores.groupby('alpha').ic.mean().idxmax()

preds = lasso_predictions[lasso_predictions.alpha==best_alpha]

lasso_r, lasso_p = spearmanr(preds.actuals, preds.predicted)

print(f'Information Coefficient (overall): {lasso_r:.3%} (p-value: {lasso_p:.4%})')

'''

Information Coefficient (overall): 3.600% (p-value: 0.0000%)

'''lasso_scores.groupby('alpha').ic.agg(['mean', 'median'])

ラッソ係数のパス

fig, axes = plt.subplots(ncols=2, sharex=True, figsize=(15, 5))

scores_by_alpha = lasso_scores.groupby('alpha').ic.agg(['mean', 'median'])

best_alpha_mean = scores_by_alpha['mean'].idxmax()

best_alpha_median = scores_by_alpha['median'].idxmax()

ax = sns.lineplot(x='alpha', y='ic', data=lasso_scores, estimator=np.mean, label='Mean', ax=axes[0])

scores_by_alpha['median'].plot(logx=True, ax=axes[0], label='Median')

axes[0].axvline(best_alpha_mean, ls='--', c='k', lw=1, label='Max. Mean')

axes[0].axvline(best_alpha_median, ls='-.', c='k', lw=1, label='Max. Median')

axes[0].legend()

axes[0].set_xscale('log')

axes[0].set_xlabel('Alpha')

axes[0].set_ylabel('Information Coefficient')

axes[0].set_title('Cross Validation Performance')

lasso_coeffs.plot(logx=True, legend=False, ax=axes[1], title='Lasso Coefficient Path')

axes[1].axvline(best_alpha_mean, ls='--', c='k', lw=1, label='Max. Mean')

axes[1].axvline(best_alpha_median, ls='-.', c='k', lw=1, label='Max. Median')

axes[1].set_xlabel('Alpha')

axes[1].set_ylabel('Coefficient Value')

fig.suptitle('Lasso Results', fontsize=14)

fig.tight_layout()

fig.subplots_adjust(top=.9)

sns.despine();

ラッソIC分布と上位10特徴量

best_alpha = lasso_scores.groupby('alpha').ic.mean().idxmax()

fig, axes = plt.subplots(ncols=2, figsize=(15, 5))

plot_ic_distribution(lasso_scores[lasso_scores.alpha==best_alpha], ax=axes[0])

axes[0].set_title('Daily Information Coefficients')

top_coeffs = lasso_coeffs.loc[best_alpha].abs().sort_values().head(10).index

top_coeffs.tolist()

lasso_coeffs.loc[best_alpha, top_coeffs].sort_values().plot.barh(ax=axes[1], title='Top 10 Coefficients')

sns.despine()

fig.tight_layout();

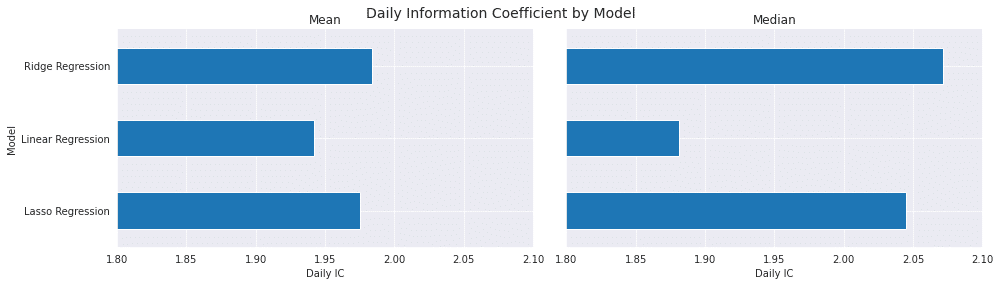

結果の比較

best_ridge_alpha = ridge_scores.groupby('alpha').ic.mean().idxmax()

best_ridge_preds = ridge_predictions[ridge_predictions.alpha==best_ridge_alpha]

best_ridge_scores = ridge_scores[ridge_scores.alpha==best_ridge_alpha]best_lasso_alpha = lasso_scores.groupby('alpha').ic.mean().idxmax()

best_lasso_preds = lasso_predictions[lasso_predictions.alpha==best_lasso_alpha]

best_lasso_scores = lasso_scores[lasso_scores.alpha==best_lasso_alpha]df = pd.concat([lr_scores.assign(Model='Linear Regression'),

best_ridge_scores.assign(Model='Ridge Regression'),

best_lasso_scores.assign(Model='Lasso Regression')]).drop('alpha', axis=1)

df.columns = ['IC', 'RMSE', 'Model']scores = df.groupby('Model').IC.agg(['mean', 'median'])

fig, axes = plt.subplots(ncols=2, figsize=(14,4), sharey=True, sharex=True)

scores['mean'].plot.barh(ax=axes[0], xlim=(1.85, 2), title='Mean')

scores['median'].plot.barh(ax=axes[1], xlim=(1.8, 2.1), title='Median')

axes[0].set_xlabel('Daily IC')

axes[1].set_xlabel('Daily IC')

fig.suptitle('Daily Information Coefficient by Model', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9)

結果は線形回帰モデルよりもリッジ回帰の方が圧倒的に良いですね(*'ω'*)

本記事のコードはそのまま使えますので、リッジ回帰のやり方はご参考にしてくださいませ(*'ω'*)

この記事が気に入ったらサポートをしてみませんか?