第10章:ベイジアンML-ダイナミックSR 第5節: 確率的ボラティリティモデル

インポートと設定

import warnings

warnings.filterwarnings('ignore')%matplotlib inline

from pathlib import Path

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormatter

import seaborn as sns

import pymc3 as pm

from pymc3.distributions.timeseries import GaussianRandomWalksns.set_style('whitegrid')

# model_path = Path('models')モデルの仮定

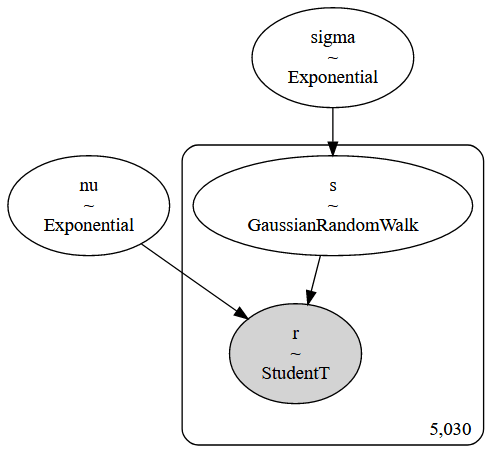

資産価格は時変ボラティリティ(日ごとの収益の変動)を持っています。一部の期間では、株価は非常に変動しやすく、他の期間では非常に安定しています。確率的ボラティリティモデルは、潜在的ボラティリティ変数を使用してこれをモデル化し、確率過程としてモデル化します。

次のモデルは、No-U-Turn Samplerの論文、Hoffman(2011)p21で説明されているモデルに似ています。

σ~Exponential(50)

v~Exponential(0.1)

s_i ~ Normal(s_{i-1}, σ^{-2})

log(r_i) ~ t(v, 0, exp(-2s_i))

ただし、rは日次リターンでsは潜在的ログボラティリティ過程

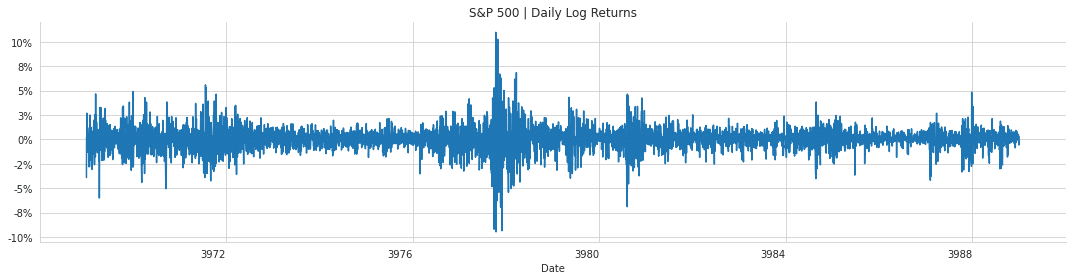

価格データの取得

今回はS&P 500を使います。

prices = pd.read_hdf('../data/assets.h5', key='sp500/stooq').loc['2000':, 'close']

log_returns = np.log(prices).diff().dropna()ax = log_returns.plot(figsize=(15, 4),

title='S&P 500 | Daily Log Returns',

rot=0)

ax.yaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

sns.despine()

plt.tight_layout();

PyMC3でモデルを特定する。

with pm.Model() as model:

step_size = pm.Exponential('sigma', 50.)

s = GaussianRandomWalk('s', sd=step_size,

shape=len(log_returns))

nu = pm.Exponential('nu', .1)

r = pm.StudentT('r', nu=nu,

lam=pm.math.exp(-2*s),

observed=log_returns)pm.model_to_graphviz(model)

モデルのフィッティング

with model:

trace = pm.sample(tune=2000,

draws=5000,

chains=4,

cores=1,

target_accept=.9)結果の評価

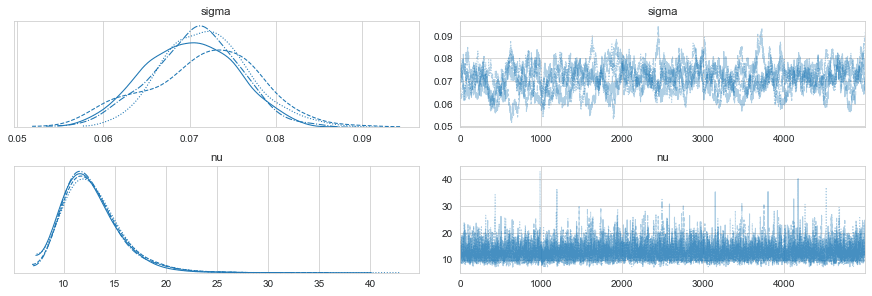

痕跡プロット

pm.traceplot(trace, varnames=['sigma', 'nu']);

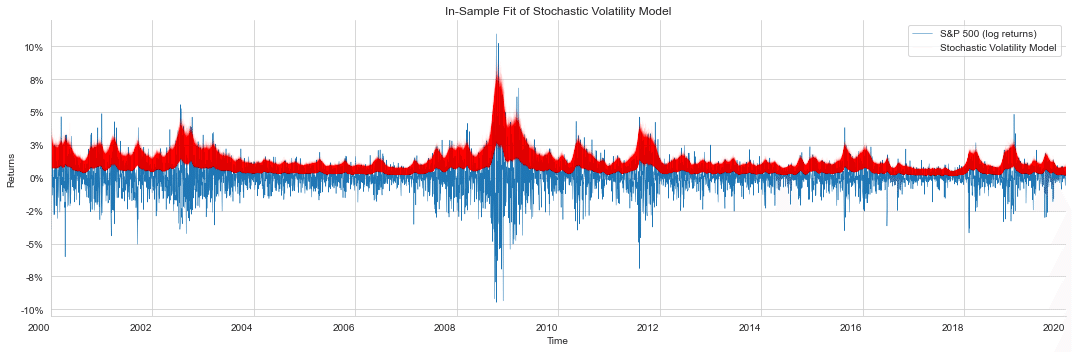

インサンプル予測

pm.trace_to_dataframe(trace).info()

'''

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 4000 entries, 0 to 3999

Columns: 5032 entries, s__0 to nu

dtypes: float64(5032)

memory usage: 153.6 MB

'''fig, ax = plt.subplots(figsize=(15, 5))

log_returns.plot(ax=ax, lw=.5, xlim=('2000', '2020'), rot=0,

title='In-Sample Fit of Stochastic Volatility Model')

ax.plot(log_returns.index, np.exp(trace[s]).T, 'r', alpha=.03, lw=.5);

ax.set(xlabel='Time', ylabel='Returns')

ax.legend(['S&P 500 (log returns)', 'Stochastic Volatility Model'])

ax.yaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

sns.despine()

fig.tight_layout();

この記事が気に入ったらサポートをしてみませんか?