第12章:戦略をブースティングする 第1節: ブースティング・ベースライン

はじめに

とうとう第12章です。ここで教師あり学習は終わって、13章以降は深層学習含めた教師なし学習をメインに取り扱います。また、教師あり学習のケースでも深層学習を取り扱ったりします。

※以下は個人的な見解になります。

この章まで出来れば機械学習及びファクター投資の知識としてはほぼ十分かと思われます。

実際、深層学習を用いたトレーディング手法はかなり研究されておりますが、難易度も高く、投資においてはブラックボックスになること自体がリスクであるので、実務上で使われるためにはかなりのハードルをクリアする必要があります。

それと比べて、ファクター投資とアンサンブルモデルによる学習は、負けた時にファクターがこの場面では効かなかった等、言い訳がつけやすく、モデルの向上もさせやすいため、難易度はどちらも高いですが、扱いやすさは断然ファクター研究の方になります。

インポートと設定

%matplotlib inline

import sys, os

import warnings

from time import time

from itertools import product

import joblib

from pathlib import Path

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormatter

from mpl_toolkits.mplot3d import Axes3D

import seaborn as sns

from xgboost import XGBClassifier

from lightgbm import LGBMClassifier

from catboost import CatBoostClassifier

from sklearn.model_selection import cross_validate

from sklearn.dummy import DummyClassifier

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier, AdaBoostClassifier, GradientBoostingClassifier

from sklearn.inspection import partial_dependence, plot_partial_dependence

from sklearn.metrics import roc_auc_scoresys.path.insert(1, os.path.join(sys.path[0], '..'))

from utils import format_timeresults_path = Path('results', 'baseline')

if not results_path.exists():

results_path.mkdir(exist_ok=True, parents=True)warnings.filterwarnings('ignore')

sns.set_style("whitegrid")

idx = pd.IndexSlice

np.random.seed(42)データの準備

4章アルファ-ファクター研究: 第一節: 特徴量エンジニアリングからデータを作成してください。

DATA_STORE = '../data/assets.h5'def get_data(start='2000', end='2018', task='classification', holding_period=1, dropna=False):

idx = pd.IndexSlice

target = f'target_{holding_period}m'

with pd.HDFStore(DATA_STORE) as store:

df = store['engineered_features']

if start is not None and end is not None:

df = df.loc[idx[:, start: end], :]

if dropna:

df = df.dropna()

y = (df[target]>0).astype(int)

X = df.drop([c for c in df.columns if c.startswith('target')], axis=1)

return y, Xカテゴリーに分解する

cat_cols = ['year', 'month', 'age', 'msize', 'sector']def factorize_cats(df, cats=['sector']):

cat_cols = ['year', 'month', 'age', 'msize'] + cats

for cat in cats:

df[cat] = pd.factorize(df[cat])[0]

df.loc[:, cat_cols] = df.loc[:, cat_cols].fillna(-1).astype(int)

return dfONE-HOT エンコーディング

One-hotに関してはこちら

以下引用

デジタル回路において、one-hot(ワン・ホット)は1つだけHigh(1)であり、他はLow(0)であるようなビット列のことを指す。 類似のものとして、0が1つだけで、他がすべて1であるようなビット列をone-cold(ワン・コールド)と呼ぶことがある。

def get_one_hot_data(df, cols=cat_cols[:-1]):

df = pd.get_dummies(df,

columns=cols + ['sector'],

prefix=cols + [''],

prefix_sep=['_'] * len(cols) + [''])

return df.rename(columns={c: c.replace('.0', '') for c in df.columns})ホールドアウト法

ホールドアウト法に関しては、こちら

以下引用です。

教師あり学習を行う上で、モデルを作成し評価するための基本的な手法

教師ありデータを学習データとテストデータに分割する。

学習データでモデルを作成し、テストデータで性能を図る。

より効果的な方法として、データを学習データ、検証データ、テストデータと3つに分割し、検証データによって複数のモデルを評価・選択して最終的にテストデータで汎化誤差を評価する方法がある。

よく取られる手法です。

def get_holdout_set(target, features, period=6):

idx = pd.IndexSlice

label = target.name

dates = np.sort(y.index.get_level_values('date').unique())

cv_start, cv_end = dates[0], dates[-period - 2]

holdout_start, holdout_end = dates[-period - 1], dates[-1]

df = features.join(target.to_frame())

train = df.loc[idx[:, cv_start: cv_end], :]

y_train, X_train = train[label], train.drop(label, axis=1)

test = df.loc[idx[:, holdout_start: holdout_end], :]

y_test, X_test = test[label], test.drop(label, axis=1)

return y_train, X_train, y_test, X_testデータの読み込み

y, features = get_data()

X_dummies = get_one_hot_data(features)

X_factors = factorize_cats(features)X_factors.info()

'''

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 358914 entries, ('A', Timestamp('2001-01-31 00:00:00')) to ('ZUMZ', Timestamp('2018-02-28 00:00:00'))

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 return_1m 358914 non-null float64

1 return_2m 358914 non-null float64

2 return_3m 358914 non-null float64

3 return_6m 358914 non-null float64

4 return_9m 358914 non-null float64

5 return_12m 358914 non-null float64

6 Mkt-RF 358914 non-null float64

7 SMB 358914 non-null float64

8 HML 358914 non-null float64

9 RMW 358914 non-null float64

10 CMA 358914 non-null float64

11 momentum_2 358914 non-null float64

12 momentum_3 358914 non-null float64

13 momentum_6 358914 non-null float64

14 momentum_9 358914 non-null float64

15 momentum_12 358914 non-null float64

16 year 358914 non-null int64

17 month 358914 non-null int64

18 return_1m_t-1 357076 non-null float64

19 return_1m_t-2 355238 non-null float64

20 return_1m_t-3 353400 non-null float64

21 return_1m_t-4 351562 non-null float64

22 return_1m_t-5 349724 non-null float64

23 return_1m_t-6 347886 non-null float64

24 age 358914 non-null int64

25 msize 358914 non-null int64

26 sector 358914 non-null int64

dtypes: float64(22), int64(5)

memory usage: 85.3+ MB

'''y_clean, features_clean = get_data(dropna=True)

X_dummies_clean = get_one_hot_data(features_clean)

X_factors_clean = factorize_cats(features_clean)交差検証セットアップ

カスタム時系列Kフォールド生成器

class OneStepTimeSeriesSplit:

"""Generates tuples of train_idx, test_idx pairs

Assumes the index contains a level labeled 'date'"""

def __init__(self, n_splits=3, test_period_length=1, shuffle=False):

self.n_splits = n_splits

self.test_period_length = test_period_length

self.shuffle = shuffle

@staticmethod

def chunks(l, n):

for i in range(0, len(l), n):

yield l[i:i + n]

def split(self, X, y=None, groups=None):

unique_dates = (X.index

.get_level_values('date')

.unique()

.sort_values(ascending=False)

[:self.n_splits*self.test_period_length])

dates = X.reset_index()[['date']]

for test_date in self.chunks(unique_dates, self.test_period_length):

train_idx = dates[dates.date < min(test_date)].index

test_idx = dates[dates.date.isin(test_date)].index

if self.shuffle:

np.random.shuffle(list(train_idx))

yield train_idx, test_idx

def get_n_splits(self, X, y, groups=None):

return self.n_splitscv = OneStepTimeSeriesSplit(n_splits=12,

test_period_length=1,

shuffle=False)run_time = {}CV 評価関数

metrics = {'balanced_accuracy': 'Accuracy' ,

'roc_auc': 'AUC',

'neg_log_loss': 'Log Loss',

'f1_weighted': 'F1',

'precision_weighted': 'Precision',

'recall_weighted': 'Recall'

}def run_cv(clf, X=X_dummies, y=y, metrics=metrics, cv=cv, fit_params=None, n_jobs=-1):

start = time()

scores = cross_validate(estimator=clf,

X=X,

y=y,

scoring=list(metrics.keys()),

cv=cv,

return_train_score=True,

n_jobs=n_jobs,

verbose=1,

fit_params=fit_params)

duration = time() - start

return scores, durationCV結果ハンドラー関数

CVの結果を操作してプロットする補助関数

def stack_results(scores):

columns = pd.MultiIndex.from_tuples(

[tuple(m.split('_', 1)) for m in scores.keys()],

names=['Dataset', 'Metric'])

data = np.array(list(scores.values())).T

df = (pd.DataFrame(data=data,

columns=columns)

.iloc[:, 2:])

results = pd.melt(df, value_name='Value')

results.Metric = results.Metric.apply(lambda x: metrics.get(x))

results.Dataset = results.Dataset.str.capitalize()

return resultsdef plot_result(df, model=None, fname=None):

m = list(metrics.values())

g = sns.catplot(x='Dataset',

y='Value',

hue='Dataset',

col='Metric',

data=df,

col_order=m,

order=['Train', 'Test'],

kind="box",

col_wrap=3,

sharey=False,

height=4, aspect=1.2)

df = df.groupby(['Metric', 'Dataset']).Value.mean().unstack().loc[m]

for i, ax in enumerate(g.axes.flat):

s = f"Train: {df.loc[m[i], 'Train']:>7.4f}\nTest: {df.loc[m[i], 'Test'] :>7.4f}"

ax.text(0.05, 0.85, s, fontsize=10, transform=ax.transAxes,

bbox=dict(facecolor='white', edgecolor='grey', boxstyle='round,pad=0.5'))

g.fig.suptitle(model, fontsize=16)

g.fig.subplots_adjust(top=.9)

if fname:

g.savefig(fname, dpi=300);ベースライン分類器

dummy_clf = DummyClassifier(strategy='stratified',

random_state=42)algo = 'dummy_clf'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

dummy_cv_result, run_time[algo] = run_cv(dummy_clf)

joblib.dump(dummy_cv_result, fname)

else:

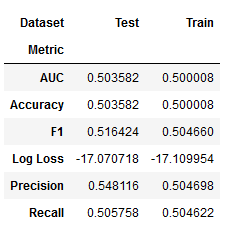

dummy_cv_result = joblib.load(fname)dummy_result = stack_results(dummy_cv_result)

dummy_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

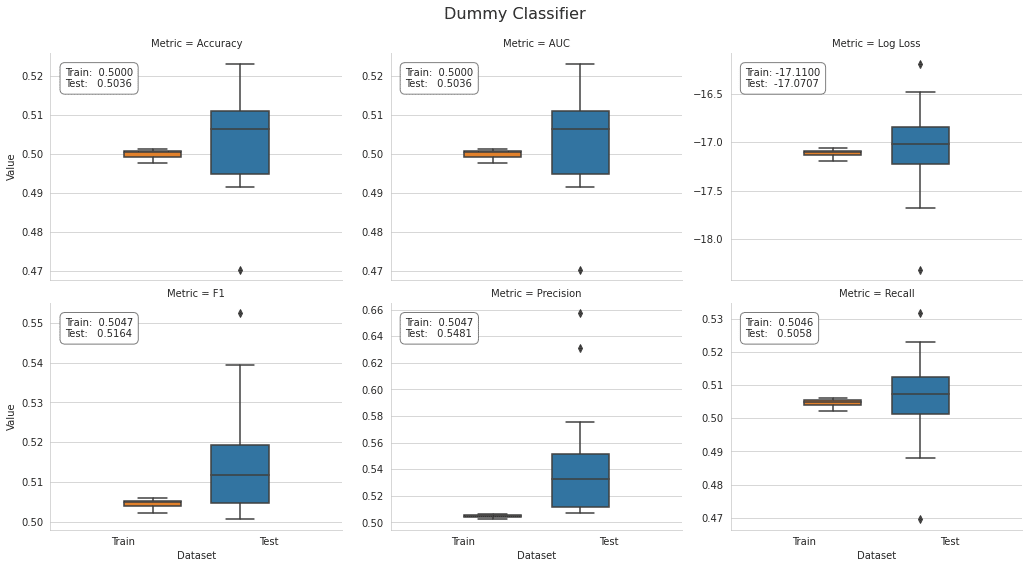

plot_result(dummy_result, model='Dummy Classifier')

ランダムフォレスト

設定

rf_clf = RandomForestClassifier(n_estimators=100,

criterion='gini',

max_depth=None,

min_samples_split=2,

min_samples_leaf=1,

min_weight_fraction_leaf=0.0,

max_features='auto',

max_leaf_nodes=None,

min_impurity_decrease=0.0,

min_impurity_split=None,

bootstrap=True,

oob_score=True,

n_jobs=-1,

random_state=42,

verbose=1)交差検証

algo = 'random_forest'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

rf_cv_result, run_time[algo] = run_cv(rf_clf, y=y_clean, X=X_dummies_clean)

joblib.dump(rf_cv_result, fname)

else:

rf_cv_result = joblib.load(fname)結果のプロット

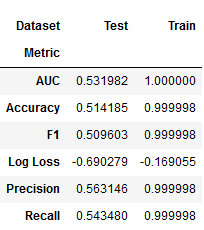

rf_result = stack_results(rf_cv_result)

rf_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

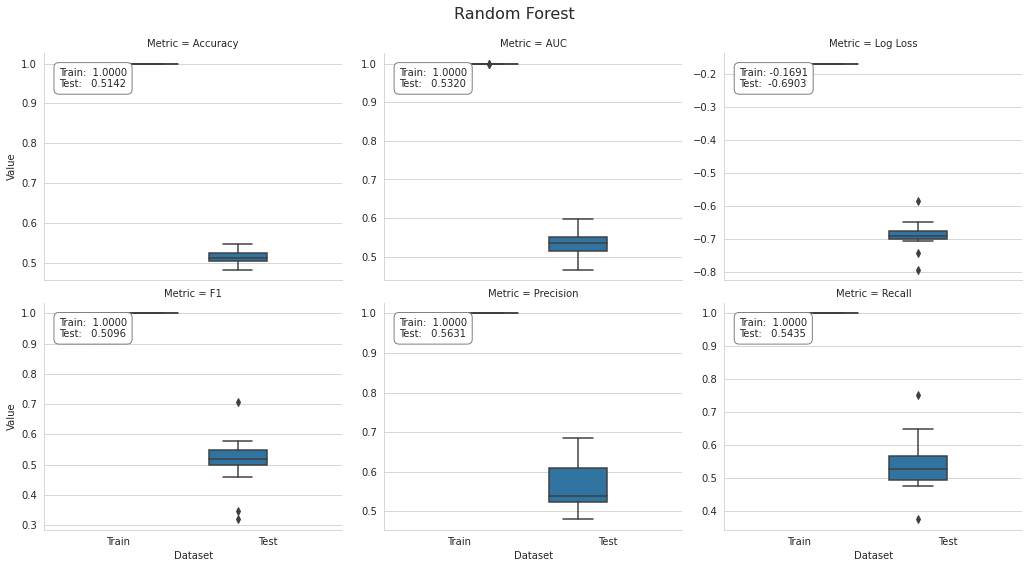

plot_result(rf_result, model='Random Forest')

AdaBoost

前の章で説明したように、max_depthへの変更は、min_samples_splitなどの調整を使用して、適切な正則化制約と組み合わせる必要があります。

base_estimator = DecisionTreeClassifier(criterion='gini',

splitter='best',

max_depth=1,

min_samples_split=2,

min_samples_leaf=20,

min_weight_fraction_leaf=0.0,

max_features=None,

random_state=None,

max_leaf_nodes=None,

min_impurity_decrease=0.0,

min_impurity_split=None,

class_weight=None)設定

ada_clf = AdaBoostClassifier(base_estimator=base_estimator,

n_estimators=100,

learning_rate=1.0,

algorithm='SAMME.R',

random_state=42)交差検証

algo = 'adaboost'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

ada_cv_result, run_time[algo] = run_cv(ada_clf, y=y_clean, X=X_dummies_clean)

joblib.dump(ada_cv_result, fname)

else:

ada_cv_result = joblib.load(fname)結果のプロット

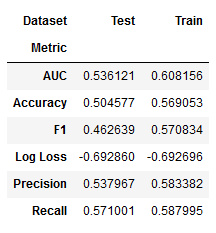

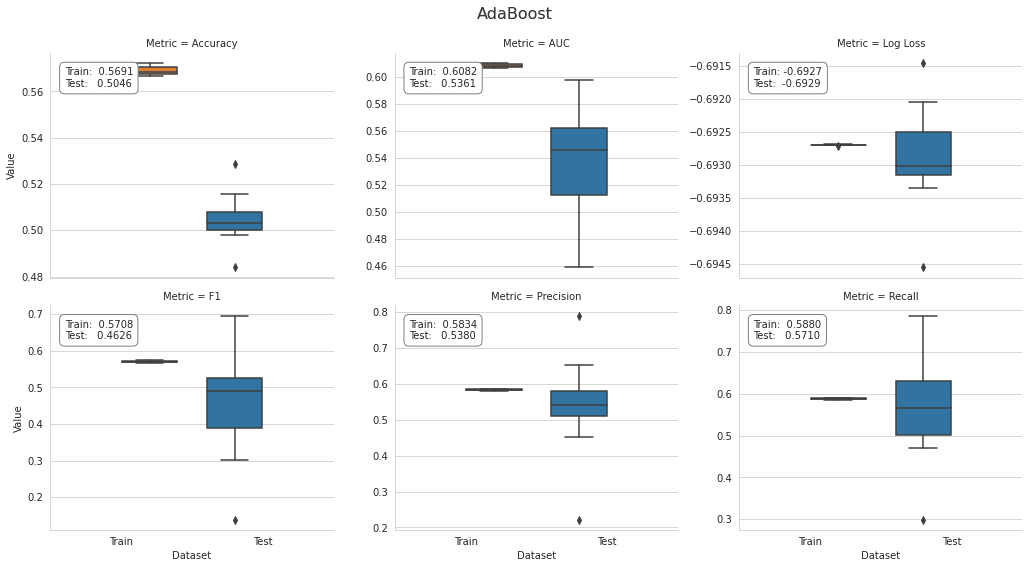

ada_result = stack_results(ada_cv_result)

ada_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

plot_result(ada_result, model='AdaBoost')

GradientBoostingClassifier

設定

gb_clf = GradientBoostingClassifier(loss='deviance', # deviance = logistic reg; exponential: AdaBoost

learning_rate=0.1, # shrinks the contribution of each tree

n_estimators=100, # number of boosting stages

subsample=1.0, # fraction of samples used t fit base learners

criterion='friedman_mse', # measures the quality of a split

min_samples_split=2,

min_samples_leaf=1,

min_weight_fraction_leaf=0.0, # min. fraction of sum of weights

max_depth=3, # opt value depends on interaction

min_impurity_decrease=0.0,

min_impurity_split=None,

init=None,

random_state=None,

max_features=None,

verbose=0,

max_leaf_nodes=None,

warm_start=False,

presort='auto',

validation_fraction=0.1,

n_iter_no_change=None,

tol=0.0001)交差検証

algo = 'sklearn_gbm'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

gb_cv_result, run_time[algo] = run_cv(gb_clf, y=y_clean, X=X_dummies_clean)

joblib.dump(gb_cv_result, fname)

else:

gb_cv_result = joblib.load(fname)結果のプロット

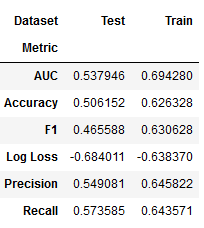

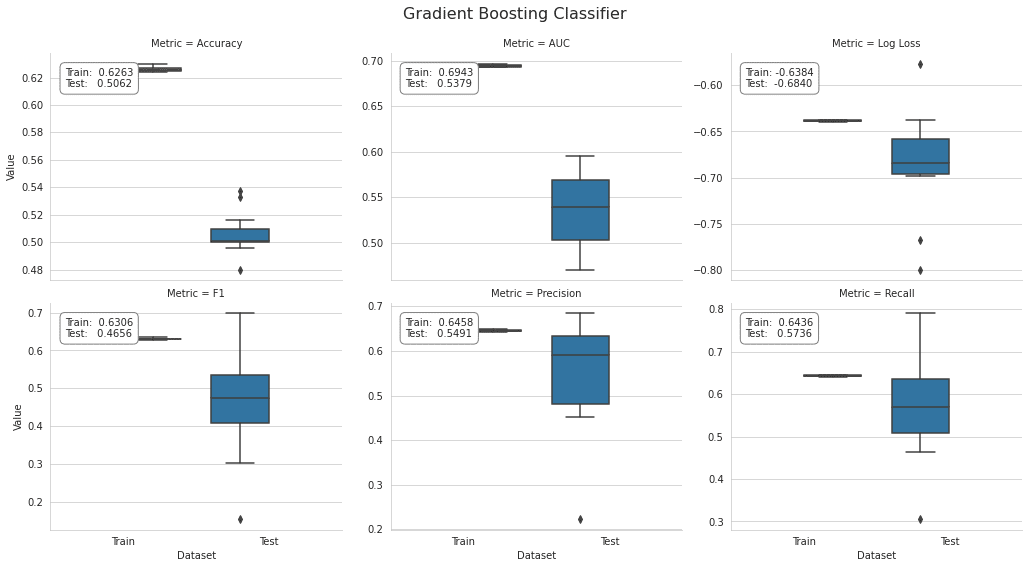

gb_result = stack_results(gb_cv_result)

gb_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

plot_result(gb_result, model='Gradient Boosting Classifier')

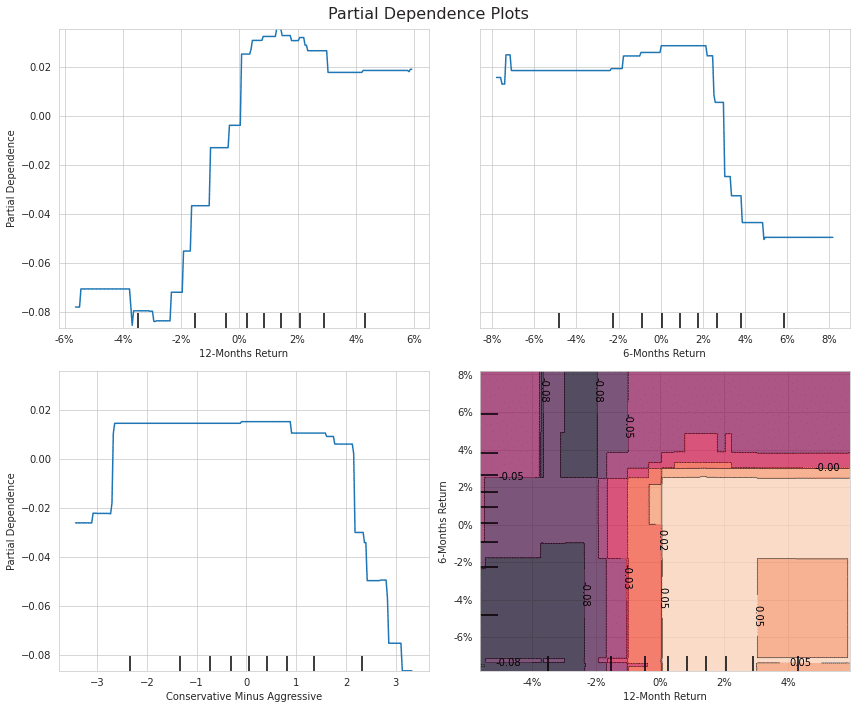

Partial Dependence Plot

こちらの記事参考。

以下引用です。

各変数の重要度がわかったら、次に行うべきは重要な変数とアウトカムの関係を見ることだと思います。 ただ、一般にブラックボックスモデルにおいてインプットとアウトカムの関係は非常に複雑で、可視化することは困難です。

そこで、複雑な関係を要約する手法の一つにPartial Dependence Plot(PDP)があります。PDPは興味のある変数以外の影響を周辺化して消してしまうことで、インプットとアウトカムの関係を単純化しようというものです。

X_ = X_factors_clean.drop(['year', 'month'], axis=1)fname = results_path / f'{algo}_model.joblib'

if not Path(fname).exists():

gb_clf.fit(y=y_clean, X=X_)

joblib.dump(gb_clf, fname)

else:

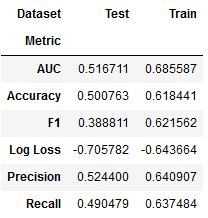

gb_clf = joblib.load(fname)# mean accuracy

gb_clf.score(X=X_, y=y_clean)

'''

0.5611655700281992

'''y_score = gb_clf.predict_proba(X_)[:, 1]

roc_auc_score(y_score=y_score, y_true=y_clean)

'''

0.5640006909636653

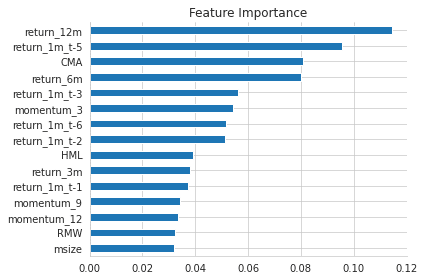

'''特徴量重要度

(pd.Series(gb_clf.feature_importances_,

index=X_.columns)

.sort_values(ascending=False)

.head(15)).sort_values().plot.barh(title='Feature Importance')

sns.despine()

plt.tight_layout();

One-wayとTwo-way PDP

fig, axes = plt.subplots(nrows=2, ncols=2, figsize=(12, 10))

plot_partial_dependence(

estimator=gb_clf,

X=X_,

features=['return_12m', 'return_6m', 'CMA', ('return_12m', 'return_6m')],

percentiles=(0.05, 0.95),

n_jobs=-1,

n_cols=2,

response_method='decision_function',

grid_resolution=250,

ax=axes)

for i, j in product([0, 1], repeat=2):

if i!=1 or j!= 0:

axes[i][j].xaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

axes[1][1].yaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

axes[0][0].set_ylabel('Partial Dependence')

axes[1][0].set_ylabel('Partial Dependence')

axes[0][0].set_xlabel('12-Months Return')

axes[0][1].set_xlabel('6-Months Return')

axes[1][0].set_xlabel('Conservative Minus Aggressive')

axes[1][1].set_xlabel('12-Month Return')

axes[1][1].set_ylabel('6-Months Return')

fig.suptitle('Partial Dependence Plots', fontsize=16)

fig.tight_layout()

fig.subplots_adjust(top=.95)

fig.savefig('figures/partial_dep_2d', dpi=300);

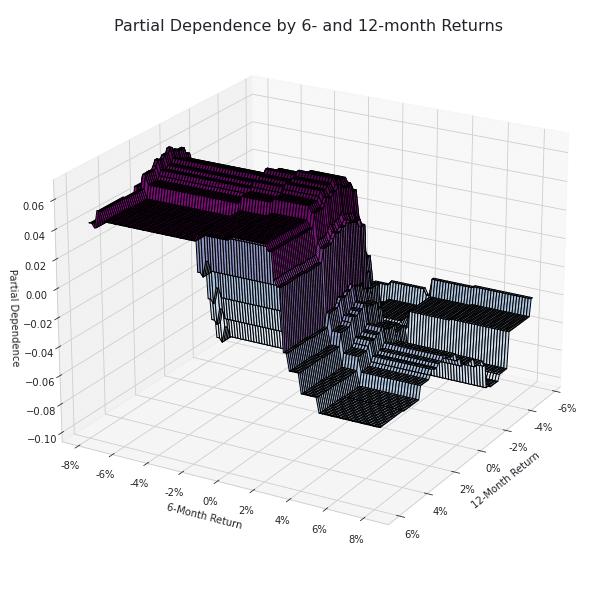

Two-way partial dependence 3D plot

targets = ['return_12m', 'return_6m']

pdp, axes = partial_dependence(estimator=gb_clf,

features=targets,

X=X_,

grid_resolution=100)

XX, YY = np.meshgrid(axes[0], axes[1])

Z = pdp[0].reshape(list(map(np.size, axes))).T

fig = plt.figure(figsize=(14, 8))

ax = Axes3D(fig)

surface = ax.plot_surface(XX, YY, Z,

rstride=1,

cstride=1,

cmap=plt.cm.BuPu,

edgecolor='k')

ax.set_xlabel('12-Month Return')

ax.set_ylabel('6-Month Return')

ax.set_zlabel('Partial Dependence')

ax.view_init(elev=22, azim=30)

ax.yaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

ax.xaxis.set_major_formatter(FuncFormatter(lambda y, _: '{:.0%}'.format(y)))

# fig.colorbar(surface)

fig.suptitle('Partial Dependence by 6- and 12-month Returns', fontsize=16)

fig.tight_layout()

fig.savefig('figures/partial_dep_3d', dpi=300)

XGBoost

設定

xgb_clf = XGBClassifier(max_depth=3, # Maximum tree depth for base learners.

learning_rate=0.1, # Boosting learning rate (xgb's "eta")

n_estimators=100, # Number of boosted trees to fit.

silent=True, # Whether to print messages while running

objective='binary:logistic', # Task and objective or custom objective function

booster='gbtree', # Select booster: gbtree, gblinear or dart

# tree_method='gpu_hist',

n_jobs=-1, # Number of parallel threads

gamma=0, # Min loss reduction for further splits

min_child_weight=1, # Min sum of sample weight(hessian) needed

max_delta_step=0, # Max delta step for each tree's weight estimation

subsample=1, # Subsample ratio of training samples

colsample_bytree=1, # Subsample ratio of cols for each tree

colsample_bylevel=1, # Subsample ratio of cols for each split

reg_alpha=0, # L1 regularization term on weights

reg_lambda=1, # L2 regularization term on weights

scale_pos_weight=1, # Balancing class weights

base_score=0.5, # Initial prediction score; global bias

random_state=42) # random seed交差検証

algo = 'xgboost'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

xgb_cv_result, run_time[algo] = run_cv(xgb_clf)

joblib.dump(xgb_cv_result, fname)

else:

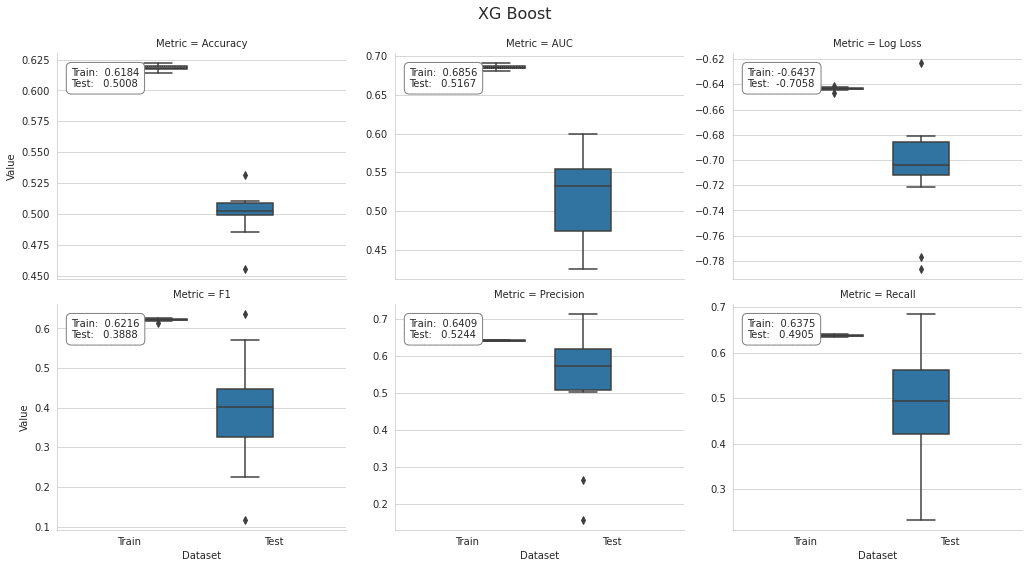

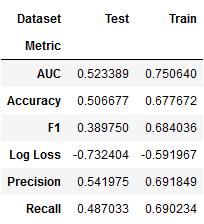

xgb_cv_result = joblib.load(fname)結果のプロット

xbg_result = stack_results(xgb_cv_result)

xbg_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

plot_result(xbg_result, model='XG Boost', fname=f'figures/{algo}_cv_result')

特徴量重要度

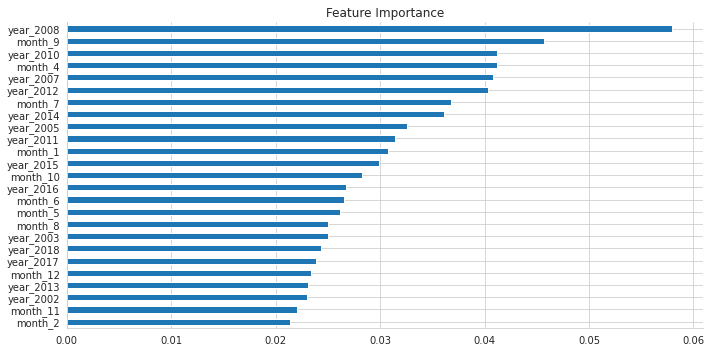

xgb_clf.fit(X=X_dummies, y=y)fi = pd.Series(xgb_clf.feature_importances_,

index=X_dummies.columns)fi.nlargest(25).sort_values().plot.barh(figsize=(10, 5),

title='Feature Importance')

sns.despine()

plt.tight_layout();

LightGBM

設定

lgb_clf = LGBMClassifier(boosting_type='gbdt',

# device='gpu',

objective='binary', # learning task

metric='auc',

num_leaves=31, # Maximum tree leaves for base learners.

max_depth=-1, # Maximum tree depth for base learners, -1 means no limit.

learning_rate=0.1, # Adaptive lr via callback override in .fit() method

n_estimators=100, # Number of boosted trees to fit

subsample_for_bin=200000, # Number of samples for constructing bins.

class_weight=None, # dict, 'balanced' or None

min_split_gain=0.0, # Minimum loss reduction for further split

min_child_weight=0.001, # Minimum sum of instance weight(hessian)

min_child_samples=20, # Minimum number of data need in a child(leaf)

subsample=1.0, # Subsample ratio of training samples

subsample_freq=0, # Frequency of subsampling, <=0: disabled

colsample_bytree=1.0, # Subsampling ratio of features

reg_alpha=0.0, # L1 regularization term on weights

reg_lambda=0.0, # L2 regularization term on weights

random_state=42, # Random number seed; default: C++ seed

n_jobs=-1, # Number of parallel threads.

silent=False,

importance_type='gain', # default: 'split' or 'gain'

)交差検証

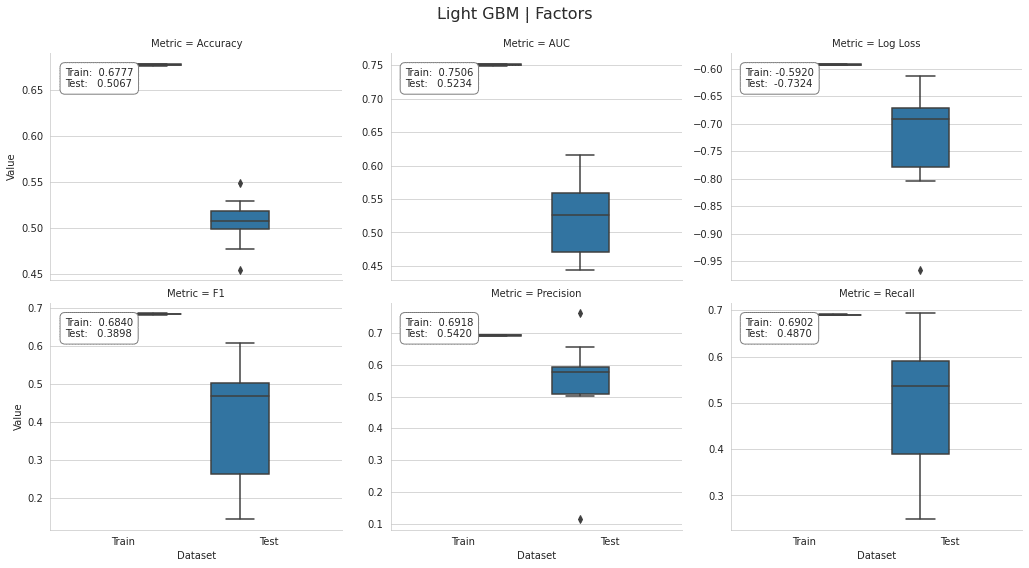

カテゴリカル特徴量を用いる

algo = 'lgb_factors'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

lgb_factor_cv_result, run_time[algo] = run_cv(lgb_clf, X=X_factors, fit_params={'categorical_feature': cat_cols})

joblib.dump(lgb_factor_cv_result, fname)

else:

lgb_factor_cv_result = joblib.load(fname)プロットの結果

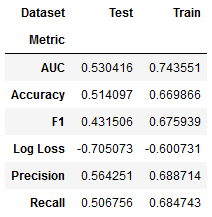

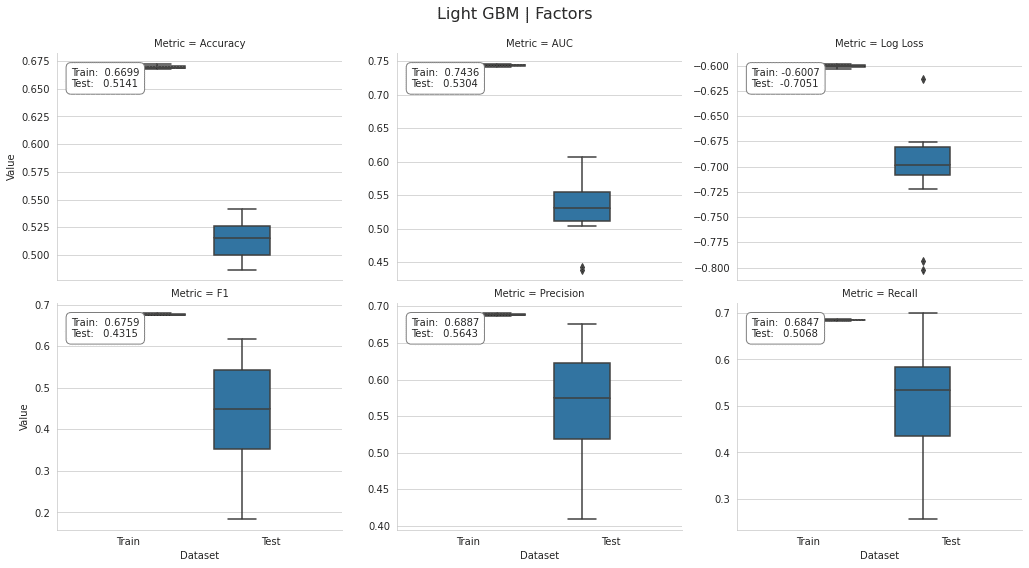

lgb_factor_result = stack_results(lgb_factor_cv_result)

lgb_factor_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

plot_result(lgb_factor_result, model='Light GBM | Factors', fname=f'figures/{algo}_cv_result')

ダミー変数を用いる

algo = 'lgb_dummies'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

lgb_dummy_cv_result, run_time[algo] = run_cv(lgb_clf)

joblib.dump(lgb_dummy_cv_result, fname)

else:

lgb_dummy_cv_result = joblib.load(fname)lgb_dummy_result = stack_results(lgb_dummy_cv_result)

lgb_dummy_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()

plot_result(lgb_dummy_result, model='Light GBM | Factors', fname=f'figures/{algo}_cv_result')

CatBoostClassifier

詳しくはこちら

設定

cat_clf = CatBoostClassifier()交差検証

s = pd.Series(X_factors.columns.tolist())

cat_cols_idx = s[s.isin(cat_cols)].index.tolist()algo = 'catboost'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

cat_cv_result, run_time[algo] = run_cv(cat_clf,

X=X_factors,

fit_params={

'cat_features': cat_cols_idx},

n_jobs=1)

joblib.dump(cat_cv_result, fname)

else:

cat_cv_result = joblib.load(fname)結果のプロット

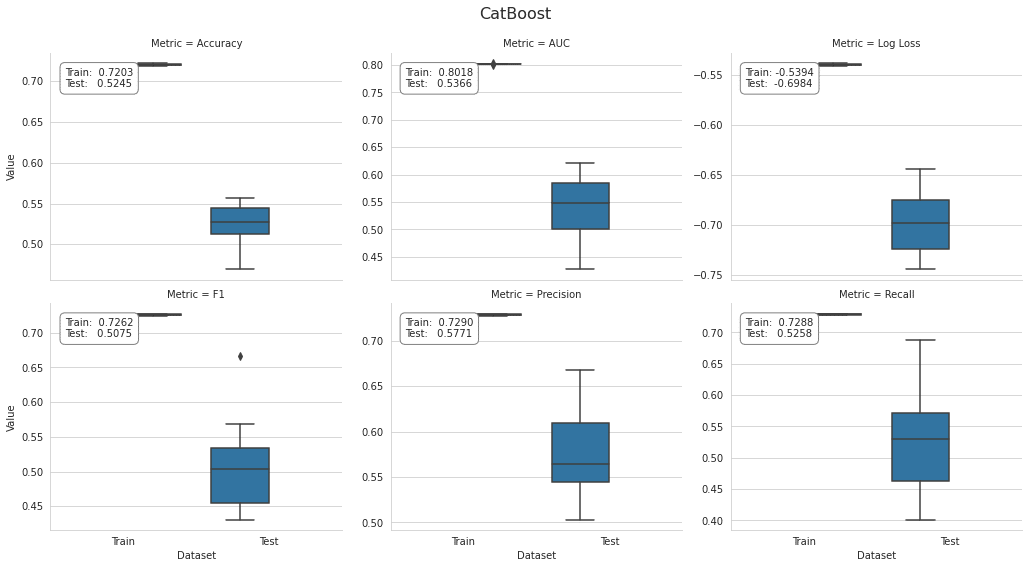

cat_result = stack_results(cat_cv_result)

cat_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()plot_result(cat_result, model='CatBoost', fname=f'figures/{algo}_cv_result')

GPU

dockerの環境にGPU入れていなかったので、私はここをスキップしました。

設定

cat_clf_gpu = CatBoostClassifier(task_type='GPU')交差検証

s = pd.Series(X_factors.columns.tolist())

cat_cols_idx = s[s.isin(cat_cols)].index.tolist()algo = 'catboost_gpu'fname = results_path / f'{algo}.joblib'

if not Path(fname).exists():

cat_gpu_cv_result, run_time[algo] = run_cv(cat_clf_gpu,

X=X_factors,

fit_params={

'cat_features': cat_cols_idx},

n_jobs=1)

joblib.dump(cat_gpu_cv_result, fname)

else:

cat_gpu_cv_result = joblib.load(fname)結果のプロット

cat_gpu_result = stack_results(cat_gpu_cv_result)

cat_gpu_result.groupby(['Metric', 'Dataset']).Value.mean().unstack()plot_result(cat_gpu_result, model='CatBoost', fname=f'figures/{algo}_cv_result')結果の比較

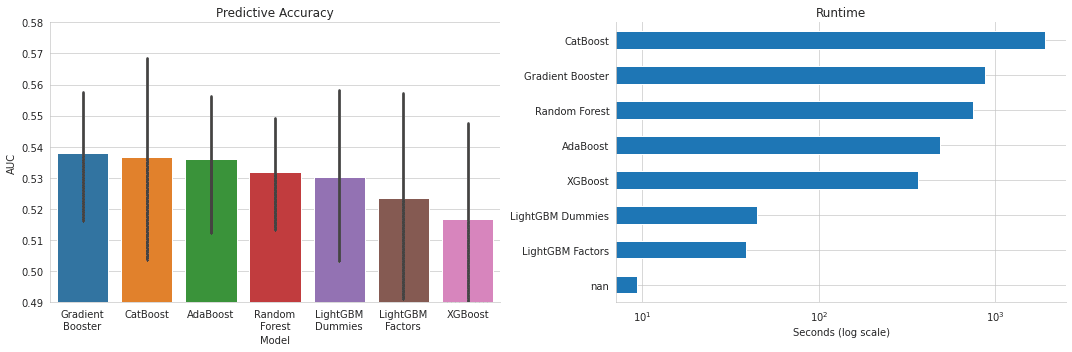

results = {'Baseline': dummy_result,

'Random Forest': rf_result,

'AdaBoost': ada_result,

'Gradient Booster': gb_result,

'XGBoost': xbg_result,

'LightGBM Dummies': lgb_dummy_result,

'LightGBM Factors': lgb_factor_result,

'CatBoost': cat_result}

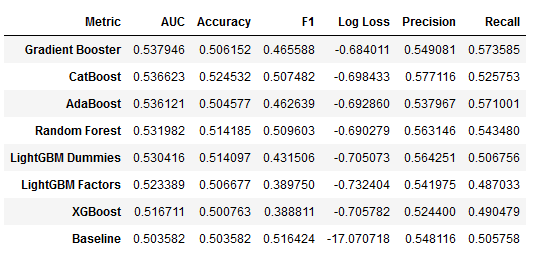

df = pd.DataFrame()

for model, result in results.items():

df = pd.concat([df, result.groupby(['Metric', 'Dataset']

).Value.mean().unstack()['Test'].to_frame(model)], axis=1)

df.T.sort_values('AUC', ascending=False)

algo_dict = dict(zip(['dummy_clf', 'random_forest', 'adaboost', 'sklearn_gbm',

'xgboost', 'lgb_factors', 'lgb_dummies', 'catboost'],

['Baseline', 'Random Forest', 'AdaBoost', 'Gradient Booster',

'XGBoost', 'LightGBM Dummies', 'LightGBM Factors', 'CatBoost']))r = pd.Series(run_time).to_frame('t')

r.index = r.index.to_series().map(algo_dict)

r.to_csv(results_path / 'runtime.csv')auc = pd.concat([v.loc[(v.Dataset=='Test') & (v.Metric=='AUC'), 'Value'].to_frame('AUC').assign(Model=k)

for k, v in results.items()])

auc = auc[auc.Model != 'Baseline']fig, axes = plt.subplots(figsize=(15, 5), ncols=2)

idx = df.T.drop('Baseline')['AUC'].sort_values(ascending=False).index

sns.barplot(x='Model', y='AUC',

data=auc,

order=idx, ax=axes[0])

axes[0].set_xticklabels([c.replace(' ', '\n') for c in idx])

axes[0].set_ylim(.49, .58)

axes[0].set_title('Predictive Accuracy')

(r.sort_values('t')).plot.barh(title='Runtime', ax=axes[1], logx=True, legend=False)

axes[1].set_xlabel('Seconds (log scale)')

sns.despine()

fig.tight_layout();

この記事が気に入ったらサポートをしてみませんか?