第11章:ランダムフォレスト - ロングショート戦略 第1節: 決定木と株価予想

はじめに

ここでは、決定木による株価予測モデルの構築とその評価について紹介します。

決定木には回帰と分類があって、回帰モデルの代表である最小二乗法による線形モデルと分類モデルの代表であるロジスティック回帰モデルと比較します。

ここでロジスティック回帰モデルが分類モデルであるにも関わらず、回帰と呼ばれている理由は、確率値を回帰して分類問題を解くからです。

基本的な内容から入るので結構長めの内容となっておりますが、初めての方でも参考になると思います(*'ω'*)

インポートと設定

import warnings

warnings.filterwarnings('ignore')%matplotlib inline

import os, sys

from pathlib import Path

import numpy as np

from scipy.stats import spearmanr

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormatter

from matplotlib import cm

import seaborn as sns

from sklearn.tree import DecisionTreeClassifier, DecisionTreeRegressor, export_graphviz, _tree

from sklearn.linear_model import LinearRegression, LogisticRegression

from sklearn.model_selection import train_test_split, GridSearchCV, learning_curve

from sklearn.metrics import roc_auc_score, roc_curve, mean_squared_error, make_scorer

import graphviz

import statsmodels.api as smsys.path.insert(1, os.path.join(sys.path[0], '..'))

from utils import MultipleTimeSeriesCVsns.set_style('white')results_path = Path('results', 'decision_trees')

if not results_path.exists():

results_path.mkdir(parents=True)モデルデータの読み込み

第4章のアルファーファクター研究で作成したデータセットの簡略版を使用します。これは、2010-2017年の期間にQuandlが提供する毎日の株価と、さまざまな設計機能で構成されています。詳細は、前の章に書いてあります。

この章の決定木モデルは、欠落変数またはカテゴリ変数を処理する機能を備えていないため、前者を削除した後で、後者にダミーエンコーディングを適用します。

with pd.HDFStore('data.h5') as store:

data = store['us/equities/monthly']

data.info()

'''

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 56756 entries, ('A', Timestamp('2010-12-31 00:00:00')) to ('ZION', Timestamp('2017-11-30 00:00:00'))

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 atr 56756 non-null float64

1 bb_down 56756 non-null float64

2 bb_high 56756 non-null float64

3 bb_low 56756 non-null float64

4 bb_mid 56756 non-null float64

5 bb_up 56756 non-null float64

6 macd 56756 non-null float64

7 natr 56756 non-null float64

8 rsi 56756 non-null float64

9 sector 56756 non-null object

10 return_1m 56756 non-null float64

11 return_3m 56756 non-null float64

12 return_6m 56756 non-null float64

13 return_12m 56756 non-null float64

14 beta 56756 non-null float64

15 SMB 56756 non-null float64

16 HML 56756 non-null float64

17 RMW 56756 non-null float64

18 CMA 56756 non-null float64

19 momentum_3 56756 non-null float64

20 momentum_6 56756 non-null float64

21 momentum_3_6 56756 non-null float64

22 momentum_12 56756 non-null float64

23 momentum_3_12 56756 non-null float64

24 year 56756 non-null int64

25 month 56756 non-null int64

26 target 56756 non-null float64

dtypes: float64(24), int64(2), object(1)

memory usage: 12.0+ MB

'''単純回帰木予測

ここでは一か月後予測をします。

X2 = data.loc[:, ['target', 'return_1m']]

X2.columns = ['y', 't-1']

X2['t-2'] = data.groupby(level='ticker').return_1m.shift()

X2 = X2.dropna()

X2.info()

'''

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 56186 entries, ('A', Timestamp('2011-01-31 00:00:00')) to ('ZION', Timestamp('2017-11-30 00:00:00'))

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 y 56186 non-null float64

1 t-1 56186 non-null float64

2 t-2 56186 non-null float64

dtypes: float64(3)

memory usage: 1.5+ MB

'''y2 = X2.y

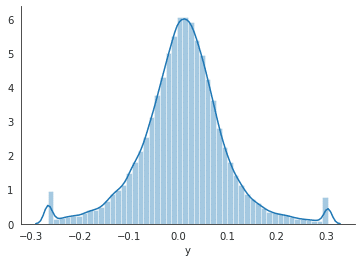

X2 = X2.drop('y', axis=1)データを見てみる

sns.distplot(y2)

sns.despine();

ツリーの設定

reg_tree_t2 = DecisionTreeRegressor(criterion='mse',

splitter='best',

max_depth=6,

min_samples_split=2,

min_samples_leaf=50,

min_weight_fraction_leaf=0.0,

max_features=None,

random_state=42,

max_leaf_nodes=None,

min_impurity_decrease=0.0,

min_impurity_split=None,

presort=False)訓練する

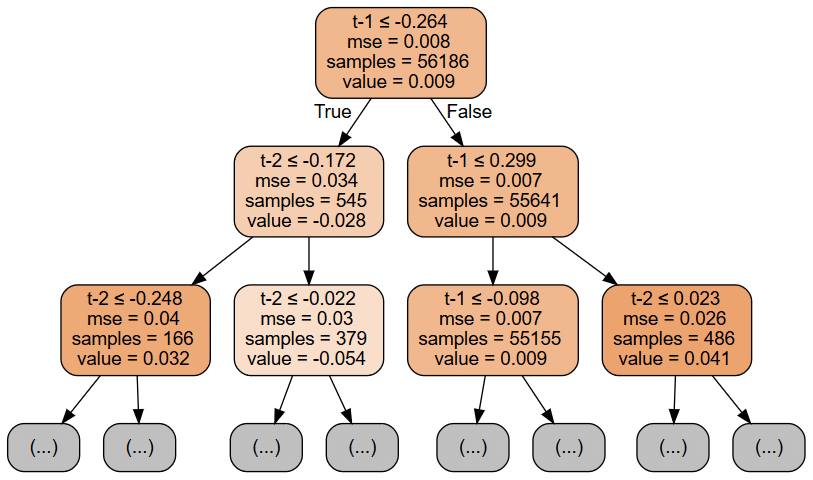

reg_tree_t2.fit(X=X2, y=y2)ツリーを視覚化する

out_file = results_path / 'reg_tree_t2.dot'

dot_data = export_graphviz(reg_tree_t2,

out_file=out_file.as_posix(),

feature_names=X2.columns,

max_depth=2,

filled=True,

rounded=True,

special_characters=True)

if out_file is not None:

dot_data = Path(out_file).read_text()

graphviz.Source(dot_data)

線形回帰と比較する

以下のOLSの概要と上の決定木の最初の2つの層を視覚化すると、モデル間の顕著な違いがわかります。 OLSモデルは、切片の3つのパラメーターと、線形仮定に沿った2つの特徴を提供します。

対照的に、上記の回帰ツリーグラフは、最初の2つのレベルの各ノードについて、データを分割するために使用される機能としきい値(機能は繰り返し使用できることに注意してください)と平均二乗誤差(MSE)の現在の値を表示します)、サンプル数、およびこれらのトレーニングサンプルに基づく予測値。

また、ツリーチャートは、2つの分割のみの後に数が31,000から65,000サンプルの間で変化するため、ノード全体のサンプルの不均一な分布を強調表示します。

statsmodels OLS

ols_model = sm.OLS(endog=y2, exog=sm.add_constant(X2))result = ols_model.fit()

print(result.summary())

'''

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.001

Model: OLS Adj. R-squared: 0.001

Method: Least Squares F-statistic: 39.02

Date: Thu, 20 Aug 2020 Prob (F-statistic): 1.17e-17

Time: 13:28:45 Log-Likelihood: 56967.

No. Observations: 56186 AIC: -1.139e+05

Df Residuals: 56183 BIC: -1.139e+05

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0088 0.000 23.412 0.000 0.008 0.009

t-1 0.0327 0.004 7.761 0.000 0.024 0.041

t-2 -0.0187 0.004 -4.437 0.000 -0.027 -0.010

==============================================================================

Omnibus: 2103.126 Durbin-Watson: 1.999

Prob(Omnibus): 0.000 Jarque-Bera (JB): 6483.607

Skew: 0.018 Prob(JB): 0.00

Kurtosis: 4.664 Cond. No. 11.5

==============================================================================

'''sklearn 線形回帰

lin_reg = LinearRegression()lin_reg.fit(X=X2,y=y2)lin_reg.intercept_

'''

0.008755441196301639

'''lin_reg.coef_

'''

array([ 0.03269516, -0.01868576])

'''識別境界 線形回帰 vs 回帰木

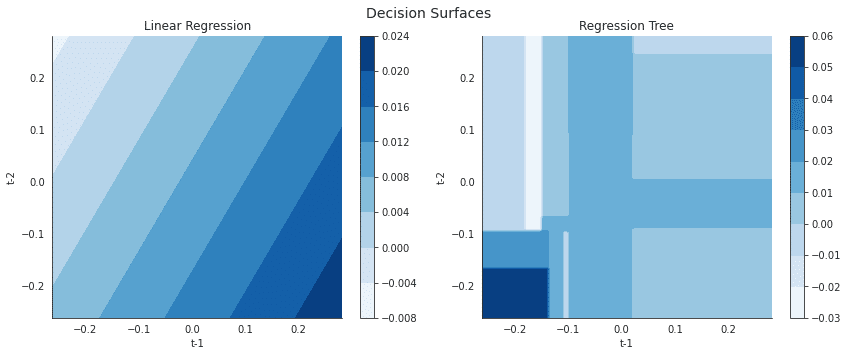

入力変数と出力の間の関係の関数形式に関するさまざまな仮定をさらに説明するために、現在のリターン予測を特徴空間の関数として、つまり遅延リターンの値の範囲の関数として視覚化できます。 次の図は、線形回帰と回帰木の1と2期間前のリターンの関数としての現在の期間のリターンを示しています。

右側の線形回帰モデルの結果は、時間差と現在のリターン間の関係の線形性を強調していますが、左側の回帰ツリーチャートは、特徴空間の再帰的分割でエンコードされた非線形関係を示しています。

t1, t2 = np.meshgrid(np.linspace(X2['t-1'].quantile(.01), X2['t-1'].quantile(.99), 100),

np.linspace(X2['t-2'].quantile(.01), X2['t-2'].quantile(.99), 100))

X_data = np.c_[t1.ravel(), t2.ravel()]fig, axes = plt.subplots(ncols=2, figsize=(12,5))

# Linear Regression

ret1 = lin_reg.predict(X_data).reshape(t1.shape)

surface1 = axes[0].contourf(t1, t2, ret1, cmap='Blues')

plt.colorbar(mappable=surface1, ax=axes[0])

# Regression Tree

ret2 = reg_tree_t2.predict(X_data).reshape(t1.shape)

surface2 = axes[1].contourf(t1, t2, ret2, cmap='Blues')

plt.colorbar(mappable=surface2, ax=axes[1])

# Format plots

titles = ['Linear Regression', 'Regression Tree']

for i, ax in enumerate(axes):

ax.set_xlabel('t-1')

ax.set_ylabel('t-2')

ax.set_title(titles[i])

fig.suptitle('Decision Surfaces', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9);

単純分類木

分類木は回帰バージョンと似ていますが、異なる点として、結果のカテゴリカルな性質(例. 0か1)の予測と損失関数の評価で異なるアプローチをとります。

回帰木は、関連する訓練サンプルの平均結果を使用して葉ノードに割り当てられた観測の応答を予測しますが、分類木は代わりにモード、つまり関連する領域の訓練サンプルの中で最も一般的なクラスを使用します。分類ツリーは、相対クラス頻度に基づいて確率的予測を生成することもできます。

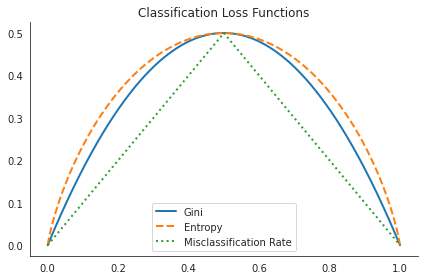

損失関数

分類木を成長させるときは、再帰的なバイナリ分割も使用しますが、平均二乗誤差の低減を使用して決定ルールの品質を評価する代わりに、誤分類率(misclassification rate)(最も大きいクラスに属していないサンプルの割合)を使用できます。

ただし、ジニ係数またはクロスエントロピーという代替指標は、分類エラー率よりもノードの純度に敏感であるため、推奨されます。ノードの純粋性は、ノード内の単一のクラスの優勢の程度を指します。単一のクラスに属する結果を持つサンプルのみを含むノードは純粋であり、特徴空間のこの特定の領域の分類が成功したことを意味します。

ここでは有名な三つの評価関数を定義します。(二値分類)

def entropy(f):

return (-f*np.log2(f) - (1-f)*np.log2(1-f))/2def gini(f):

return 2*f*(1-f)def misclassification_rate(f):

return np.where(f<=.5, f, 1-f)x = np.linspace(0, 1, 10000)

(pd.DataFrame({'Gini': gini(x),

'Entropy': entropy(x),

'Misclassification Rate': misclassification_rate(x)}, index=x)

.plot(title='Classification Loss Functions', lw=2, style=['-', '--', ':']))

sns.despine()

plt.tight_layout();

分類木の設定

clf_tree_t2 = DecisionTreeClassifier(criterion='gini',

splitter='best',

max_depth=5,

min_samples_split=1000,

min_samples_leaf=1,

min_weight_fraction_leaf=0.0,

max_features=None,

random_state=42,

max_leaf_nodes=None,

min_impurity_decrease=0.0,

min_impurity_split=None,

class_weight=None,

presort=False)y_binary = (y2>0).astype(int)

y_binary.value_counts()

'''

1 31568

0 24618

Name: y, dtype: int64

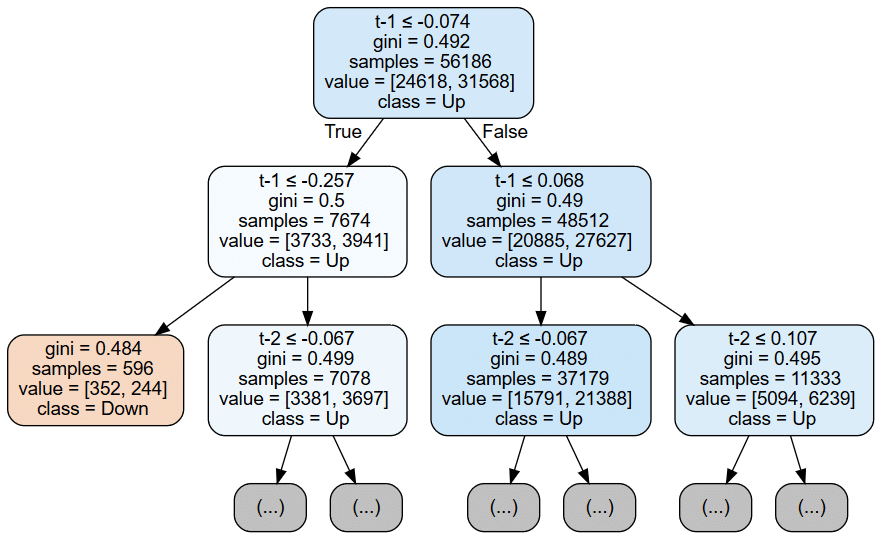

'''clf_tree_t2.fit(X=X2, y=y_binary)ツリーの視覚化

out_file = results_path / 'clf_tree_t2.dot'

dot_data = export_graphviz(clf_tree_t2,

out_file=out_file.as_posix(),

feature_names=X2.columns,

class_names=['Down', 'Up'],

max_depth=2,

filled=True,

rounded=True,

special_characters=True)

if out_file is not None:

dot_data = Path(out_file).read_text()

graphviz.Source(dot_data)

ロジスティック回帰と比較

statsmodels

log_reg_sm = sm.Logit(endog=y_binary, exog=sm.add_constant(X2))log_result = log_reg_sm.fit()

'''

Optimization terminated successfully.

Current function value: 0.685280

Iterations 4

'''print(log_result.summary())

'''

Logit Regression Results

==============================================================================

Dep. Variable: y No. Observations: 56186

Model: Logit Df Residuals: 56183

Method: MLE Df Model: 2

Date: Thu, 20 Aug 2020 Pseudo R-squ.: 0.0002871

Time: 13:29:48 Log-Likelihood: -38503.

converged: True LL-Null: -38514.

Covariance Type: nonrobust LLR p-value: 1.578e-05

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.2447 0.009 28.513 0.000 0.228 0.262

t-1 0.4548 0.097 4.698 0.000 0.265 0.644

t-2 0.0018 0.097 0.019 0.985 -0.188 0.191

==============================================================================

'''sklearn

log_reg_sk = LogisticRegression()log_reg_sk.fit(X=X2, y=y_binary)log_reg_sk.coef_

'''

array([[0.45052983, 0.0019411 ]])

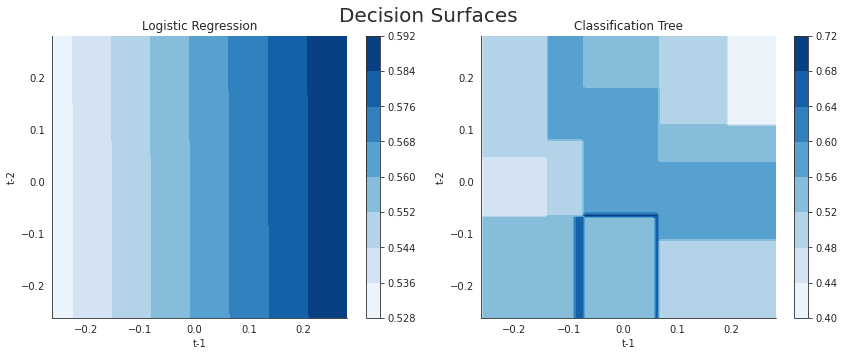

'''識別境界: 分類木 vs. ロジスティック回帰

fig, axes = plt.subplots(ncols=2, figsize=(12,5))

# Linear Regression

ret1 = log_reg_sk.predict_proba(X_data)[:, 1].reshape(t1.shape)

surface1 = axes[0].contourf(t1, t2, ret1, cmap='Blues')

plt.colorbar(mappable=surface1, ax=axes[0])

# Regression Tree

ret2 = clf_tree_t2.predict_proba(X_data)[:, 1].reshape(t1.shape)

surface2 = axes[1].contourf(t1, t2, ret2, cmap='Blues')

plt.colorbar(mappable=surface2, ax=axes[1])

# Format plots

titles = ['Logistic Regression', 'Classification Tree']

for i, ax in enumerate(axes):

ax.set_xlabel('t-1')

ax.set_ylabel('t-2')

ax.set_title(titles[i])

fig.suptitle('Decision Surfaces', fontsize=20)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9);

全ての特徴量で回帰木

80%訓練、20%テスト期間とします。

X = pd.get_dummies(data.drop('target', axis=1))

y = data.targetX_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)ツリーの設定

regression_tree = DecisionTreeRegressor(criterion='mse',

splitter='best',

max_depth=5,

min_samples_split=2,

min_samples_leaf=1,

min_weight_fraction_leaf=0.0,

max_features=None,

random_state=42,

max_leaf_nodes=None,

min_impurity_decrease=0.0,

min_impurity_split=None,

presort=False)モデルの訓練

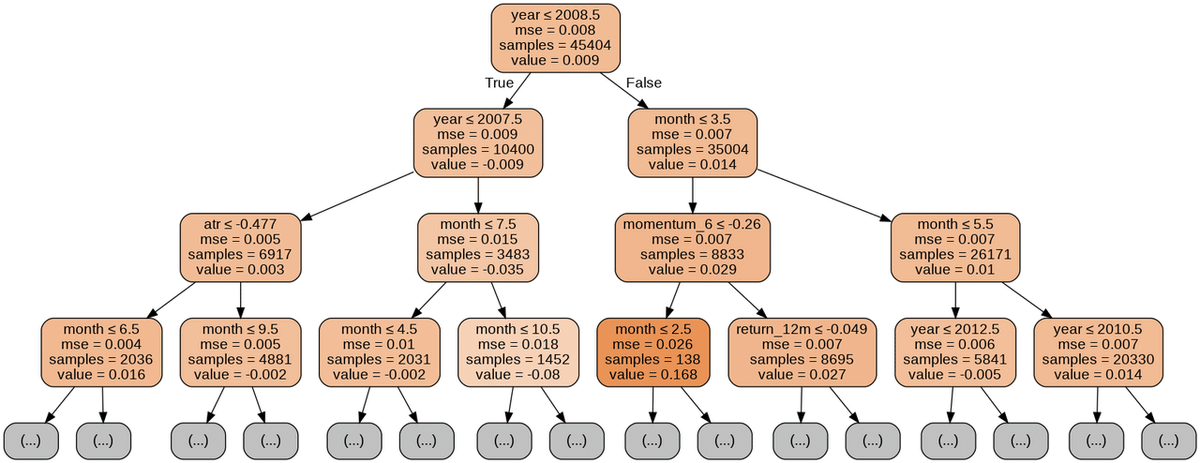

regression_tree.fit(X=X_train, y=y_train)ツリーの視覚化

out_file = results_path / 'reg_tree.dot'

dot_data = export_graphviz(regression_tree,

out_file=out_file.as_posix(),

feature_names=X_train.columns,

max_depth=3,

filled=True,

rounded=True,

special_characters=True)

if out_file is not None:

dot_data = Path(out_file).read_text()

graphviz.Source(dot_data)

テストセットの評価

y_pred = regression_tree.predict(X_test)np.sqrt(mean_squared_error(y_pred=y_pred, y_true=y_test))

'''

0.08086872759273504

'''r, p = spearmanr(y_pred, y_test)

print(f'{r*100:.2f} (p-value={p:.2%})')

'''

27.73 (p-value=0.00%)

'''全ての特徴量で分類木

y_binary = (y>0).astype(int)

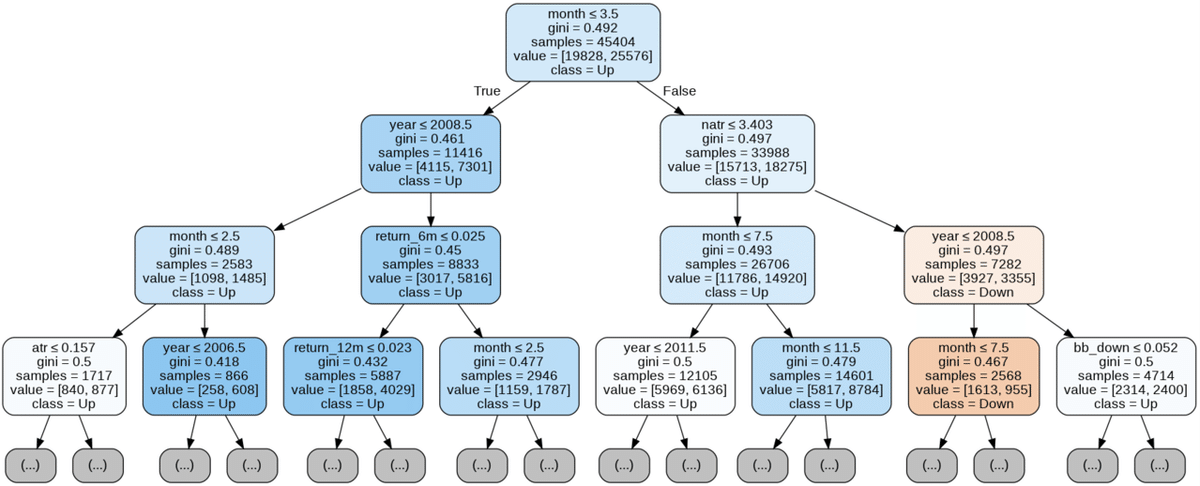

y_binary.value_counts()X_train, X_test, y_train, y_test = train_test_split(X, y_binary, test_size=0.2, random_state=42)clf = DecisionTreeClassifier(criterion='gini',

max_depth=5,

random_state=42)clf.fit(X=X_train, y=y_train)out_file = results_path / 'clf_tree.dot'

dot_data = export_graphviz(clf,

out_file=out_file.as_posix(),

feature_names=X.columns,

class_names=['Down', 'Up'],

max_depth=3,

filled=True,

rounded=True,

special_characters=True)

if out_file is not None:

dot_data = Path(out_file).read_text()

graphviz.Source(dot_data)

テストセット評価

y_score = clf.predict_proba(X=X_test)[:, 1]roc_auc_score(y_score=y_score, y_true=y_test)

'''

0.6314068026403399

'''識別パスの出力

from sklearn.tree._tree import Treedef tree_to_code(tree, feature_names):

if isinstance(tree, DecisionTreeClassifier):

model = 'clf'

elif isinstance(tree, DecisionTreeRegressor):

model = 'reg'

else:

raise ValueError('Need Regression or Classification Tree')

tree_ = tree.tree_

feature_name = [

feature_names[i] if i != _tree.TREE_UNDEFINED else "undefined!"

for i in tree_.feature

]

print("def tree({}):".format(", ".join(feature_names)))

def recurse(node, depth):

indent = " " * depth

if tree_.feature[node] != _tree.TREE_UNDEFINED:

name = feature_name[node]

threshold = tree_.threshold[node]

print(indent, f'if {name} <= {threshold:.2%}')

recurse(tree_.children_left[node], depth + 1)

print(indent, f'else: # if {name} > {threshold:.2%}')

recurse(tree_.children_right[node], depth + 1)

else:

pred = tree_.value[node][0]

val = pred[1]/sum(pred) if model == 'clf' else pred[0]

print(indent, f'return {val:.2%}')

recurse(0, 1)tree_to_code(clf_tree_t2, X2.columns)

'''

def tree(t-1, t-2):

if t-1 <= -7.44%

if t-1 <= -25.72%

return 40.94%

else: # if t-1 > -25.72%

if t-2 <= -6.72%

if t-1 <= -8.81%

if t-1 <= -8.88%

return 55.26%

else: # if t-1 > -8.88%

return 23.08%

else: # if t-1 > -8.81%

return 64.47%

else: # if t-2 > -6.72%

if t-1 <= -13.61%

if t-2 <= 4.83%

return 44.72%

else: # if t-2 > 4.83%

return 50.09%

else: # if t-1 > -13.61%

if t-2 <= 8.26%

return 51.19%

else: # if t-2 > 8.26%

return 56.97%

else: # if t-1 > -7.44%

if t-1 <= 6.76%

if t-2 <= -6.66%

if t-1 <= 6.15%

if t-1 <= -7.16%

return 72.22%

else: # if t-1 > -7.16%

return 54.31%

else: # if t-1 > 6.15%

return 66.46%

else: # if t-2 > -6.66%

if t-2 <= -6.11%

return 68.22%

else: # if t-2 > -6.11%

if t-2 <= 17.86%

return 57.84%

else: # if t-2 > 17.86%

return 53.04%

else: # if t-1 > 6.76%

if t-2 <= 10.66%

if t-2 <= -10.81%

if t-1 <= 28.33%

return 50.88%

else: # if t-1 > 28.33%

return 62.29%

else: # if t-2 > -10.81%

if t-2 <= 3.57%

return 57.25%

else: # if t-2 > 3.57%

return 53.67%

else: # if t-2 > 10.66%

if t-1 <= 18.83%

return 51.39%

else: # if t-1 > 18.83%

return 43.17%

'''過学習、正則化とパラメーターチューニング

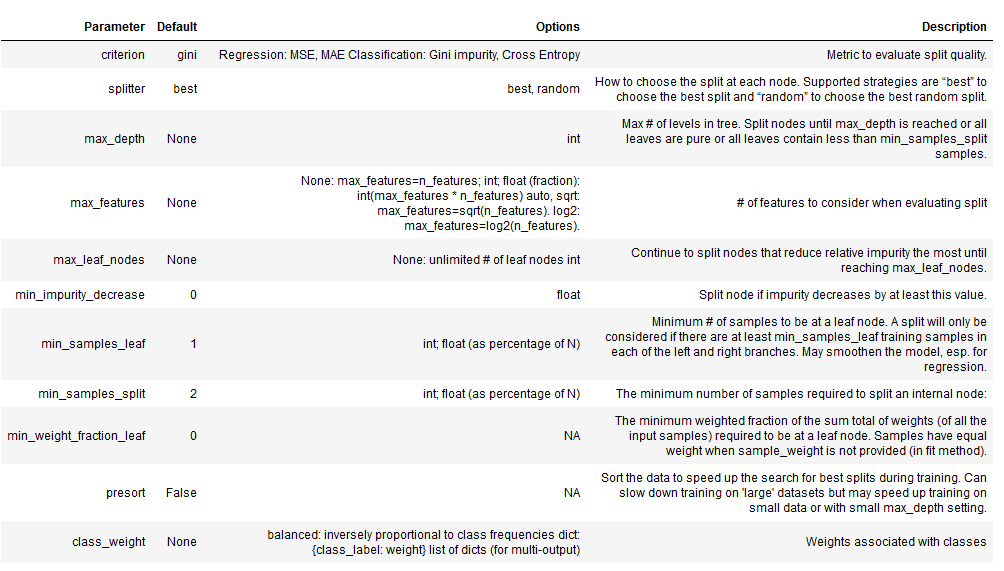

ここでパラメーターチューニングするために、決定木にどんなパラメーターがあるのかについて見ていきましょう。

max_depthパラメーターは、連続する分割の数にハード制限を課し、ツリーの成長を制限する最も簡単な方法を表します。

min_samples_splitおよびmin_samples_leafパラメータは、ツリーの成長を制限するための代替のデータ駆動型の方法です。これらのパラメーターは、連続する分割の数に厳しい制限を課すのではなく、データをさらに分割するために必要なサンプルの最小数を制御します。後者は葉ごとに特定の数のサンプルを保証しますが、前者は分割によって非常に不均一な分布が生じる場合、非常に小さな葉を作成できます。パラメーター値が小さいとオーバーフィッティングが容易になりますが、数値が大きいとツリーがデータの信号を学習できなくなる可能性があります。

多くの場合、デフォルト値は非常に低いため、交差検証を使用して潜在的な値の範囲を調査する必要があります。絶対値ではなく、フロート(float)を使用してパーセンテージを示すこともできます。

交差検定パラメーター

n_splits = 10

train_period_length = 60

test_period_length = 6

lookahead = 1

cv = MultipleTimeSeriesCV(n_splits=n_splits,

train_period_length=train_period_length,

test_period_length=test_period_length,

lookahead=lookahead)max_depths = range(1, 16)GridSearchCVを利用して最適な木を探す

パラメーターグリッドの定義

param_grid = {'max_depth': [2, 3, 4, 5, 6, 7, 8, 10, 12, 15],

'min_samples_leaf': [5, 25, 50, 100],

'max_features': ['sqrt', 'auto']}分類木

clf = DecisionTreeClassifier(random_state=42)次に、GridSearchCVオブジェクトをインスタンス化して、推定子オブジェクトとパラメーターグリッドを提供するとともに、スコアリングメソッドと交差検証の選択肢を初期化メソッドに提供します。カスタムOneStepTimeSeriesSplitクラスのオブジェクトを使用し、cvパラメーターに10倍を使用するように初期化し、スコアリングをroc_aucメトリックに設定します。 n_jobsパラメーターを使用して検索を並列化し、refit = Trueを設定することにより、最適なハイパーパラメーターを使用するトレーニング済みモデルを自動的に取得できます。

gridsearch_clf = GridSearchCV(estimator=clf,

param_grid=param_grid,

scoring='roc_auc',

n_jobs=-1,

cv=cv,

refit=True,

return_train_score=True)gridsearch_clf.fit(X=X, y=y_binary)

'''

GridSearchCV(cv=<utils.MultipleTimeSeriesCV object at 0x7f17dc1cb950>,

estimator=DecisionTreeClassifier(random_state=42), n_jobs=-1,

param_grid={'max_depth': [2, 3, 4, 5, 6, 7, 8, 10, 12, 15],

'max_features': ['sqrt', 'auto'],

'min_samples_leaf': [5, 25, 50, 100]},

return_train_score=True, scoring='roc_auc')

'''訓練の過程では、GridSearchCVオブジェクトのいくつかの新しい属性を生成します。最も重要なのは、最適な設定と最高の相互検証スコアに関する情報です(先読みバイアスを回避する適切な設定を使用しています)。

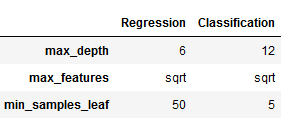

max_depthを10に、min_samples_leafを5に設定し、分割を決定するときに特徴量の総数の平方根に対応する数のみをランダムに選択すると、AUCが0.5263の最良の結果が得られます。

gridsearch_clf.best_params_

'''

{'max_depth': 12, 'max_features': 'sqrt', 'min_samples_leaf': 5}

'''gridsearch_clf.best_score_

'''

0.5263050084776537

'''カスタムICスコアの定義

def rank_correl(y, y_pred):

return spearmanr(y, y_pred)[0]

ic = make_scorer(rank_correl)回帰木

reg_tree = DecisionTreeRegressor(random_state=42)gridsearch_reg = GridSearchCV(estimator=reg_tree,

param_grid=param_grid,

scoring=ic,

n_jobs=-1,

cv=cv,

refit=True,

return_train_score=True)gridsearch_reg.fit(X=X, y=y)

'''

GridSearchCV(cv=<utils.MultipleTimeSeriesCV object at 0x7f17dc1cb950>,

estimator=DecisionTreeRegressor(random_state=42), n_jobs=-1,

param_grid={'max_depth': [2, 3, 4, 5, 6, 7, 8, 10, 12, 15],

'max_features': ['sqrt', 'auto'],

'min_samples_leaf': [5, 25, 50, 100]},

return_train_score=True, scoring=make_scorer(rank_correl))

'''gridsearch_reg.best_params_

'''

{'max_depth': 6, 'max_features': 'sqrt', 'min_samples_leaf': 50}

'''gridsearch_reg.best_score_

'''

0.08415538441512119

'''pd.DataFrame({'Regression': pd.Series(gridsearch_reg.best_params_),

'Classification': pd.Series(gridsearch_clf.best_params_)})

分類木交差検定

def get_leaves_count(tree):

t = tree.tree_

n = t.node_count

leaves = len([i for i in range(t.node_count) if t.children_left[i]== -1])

return leavestrain_scores, val_scores, leaves = {}, {}, {}

for max_depth in max_depths:

print(max_depth, end=' ', flush=True)

clf = DecisionTreeClassifier(criterion='gini',

max_depth=max_depth,

min_samples_leaf=5,

max_features='sqrt',

random_state=42)

train_scores[max_depth], val_scores[max_depth], leaves[max_depth] = [], [], []

for train_idx, test_idx in cv.split(X):

X_train, y_train, = X.iloc[train_idx], y_binary.iloc[train_idx]

X_test, y_test = X.iloc[test_idx], y_binary.iloc[test_idx]

clf.fit(X=X_train, y=y_train)

train_pred = clf.predict_proba(X=X_train)[:, 1]

train_score = roc_auc_score(y_score=train_pred, y_true=y_train)

train_scores[max_depth].append(train_score)

test_pred = clf.predict_proba(X=X_test)[:, 1]

val_score = roc_auc_score(y_score=test_pred, y_true=y_test)

val_scores[max_depth].append(val_score)

leaves[max_depth].append(get_leaves_count(clf))

clf_train_scores = pd.DataFrame(train_scores)

clf_valid_scores = pd.DataFrame(val_scores)

clf_leaves = pd.DataFrame(leaves)

'''

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

'''clf_cv_data = pd.concat([pd.melt(clf_train_scores,

var_name='Max. Depth',

value_name='ROC AUC').assign(Data='Train'),

pd.melt(clf_valid_scores,

var_name='Max. Depth',

value_name='ROC AUC').assign(Data='Valid')])回帰木交差検定

train_scores, val_scores, leaves = {}, {}, {}

for max_depth in max_depths:

print(max_depth, end=' ', flush=True)

reg_tree = DecisionTreeRegressor(max_depth=max_depth,

min_samples_leaf=50,

max_features= 'sqrt',

random_state=42)

train_scores[max_depth], val_scores[max_depth], leaves[max_depth] = [], [], []

for train_idx, test_idx in cv.split(X):

X_train, y_train, = X.iloc[train_idx], y.iloc[train_idx]

X_test, y_test = X.iloc[test_idx], y.iloc[test_idx]

reg_tree.fit(X=X_train, y=y_train)

train_pred = reg_tree.predict(X=X_train)

train_score = spearmanr(train_pred, y_train)[0]

train_scores[max_depth].append(train_score)

test_pred = reg_tree.predict(X=X_test)

val_score = spearmanr(test_pred, y_test)[0]

val_scores[max_depth].append(val_score)

leaves[max_depth].append(get_leaves_count(reg_tree))

reg_train_scores = pd.DataFrame(train_scores)

reg_valid_scores = pd.DataFrame(val_scores)

reg_leaves = pd.DataFrame(leaves)

'''

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

'''reg_cv_data = (pd.melt(reg_train_scores, var_name='Max. Depth',

value_name='IC').assign(Data='Train').append(

pd.melt(reg_valid_scores,

var_name='Max. Depth',

value_name='IC').assign(Data='Valid')))

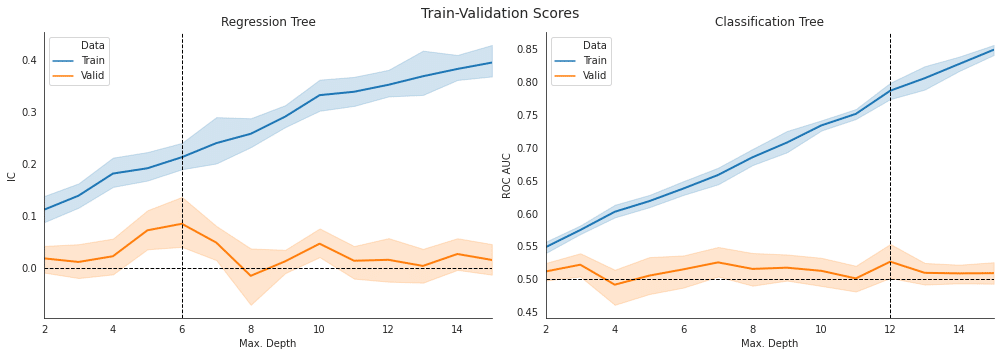

交差検定 : 回帰木 vs 分類木の比較

fig, axes = plt.subplots(ncols=2, figsize=(14, 5))

sns.lineplot(data=reg_cv_data,

x='Max. Depth', y='IC',

hue='Data', ci=95,

ax=axes[0], lw=2)

axes[0].set_title('Regression Tree')

axes[0].axvline(x=reg_valid_scores.mean().idxmax(), ls='--', c='k', lw=1)

axes[0].axhline(y=0, ls='--', c='k', lw=1)

sns.lineplot(data=clf_cv_data,

x='Max. Depth', y='ROC AUC',

hue='Data', ci=95,

ax=axes[1], lw=2)

axes[1].set_title('Classification Tree')

axes[1].axvline(x=clf_valid_scores.mean().idxmax(), ls='--', c='k', lw=1)

axes[1].axhline(y=.5, ls='--', c='k', lw=1)

for ax in axes:

ax.set_xlim(min(param_grid['max_depth']),

max(param_grid['max_depth']))

fig.suptitle(f'Train-Validation Scores', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.91)

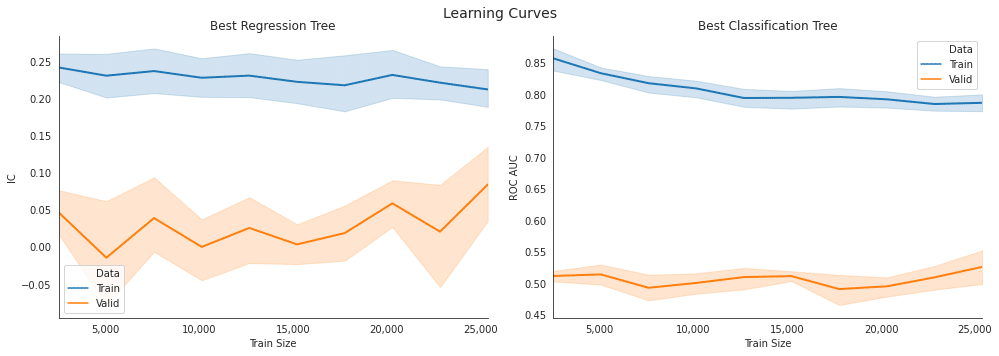

最適モデルの学習曲線

sizes = np.arange(.1, 1.01, .1)train_sizes, train_scores, valid_scores = learning_curve(gridsearch_clf.best_estimator_,

X,

y_binary,

train_sizes=sizes,

cv=cv,

scoring='roc_auc',

n_jobs=-1,

shuffle=True,

random_state=42)clf_lc_data = pd.concat([

pd.melt(pd.DataFrame(train_scores.T, columns=train_sizes),

var_name='Train Size',

value_name='ROC AUC').assign(Data='Train'),

pd.melt(pd.DataFrame(valid_scores.T, columns=train_sizes),

var_name='Train Size',

value_name='ROC AUC').assign(Data='Valid')])

clf_lc_data.info()

'''

<class 'pandas.core.frame.DataFrame'>

Int64Index: 200 entries, 0 to 99

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Train Size 200 non-null int64

1 ROC AUC 200 non-null float64

2 Data 200 non-null object

dtypes: float64(1), int64(1), object(1)

memory usage: 6.2+ KB

'''回帰木

train_sizes, train_scores, valid_scores = learning_curve(gridsearch_reg.best_estimator_,

X, y,

train_sizes=sizes,

cv=cv,

scoring=ic,

n_jobs=-1,

shuffle=True,

random_state=42)reg_lc_data = pd.concat([

pd.melt(pd.DataFrame(train_scores.T,

columns=train_sizes),

var_name='Train Size',

value_name='IC').assign(Data='Train'),

pd.melt(pd.DataFrame(valid_scores.T,

columns=train_sizes),

var_name='Train Size',

value_name='IC').assign(Data='Valid')])

reg_lc_data.info()

'''

<class 'pandas.core.frame.DataFrame'>

Int64Index: 200 entries, 0 to 99

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Train Size 200 non-null int64

1 IC 200 non-null float64

2 Data 200 non-null object

dtypes: float64(1), int64(1), object(1)

memory usage: 6.2+ KB

'''学習曲線比較

fig, axes = plt.subplots(ncols=2, figsize=(14, 5))

xmin, xmax = reg_lc_data['Train Size'].min(), reg_lc_data['Train Size'].max()

sns.lineplot(data=reg_lc_data,

x='Train Size', y='IC',

hue='Data', ci=95, ax=axes[0], lw=2)

axes[0].set_title('Best Regression Tree')

axes[0].set_ylabel('IC')

axes[0].xaxis.set_major_formatter(

FuncFormatter(lambda x, _: '{:,.0f}'.format(x)))

sns.lineplot(data=clf_lc_data,

x='Train Size',

y='ROC AUC',

hue='Data',

ci=95,

ax=axes[1],

lw=2)

axes[1].set_title('Best Classification Tree')

axes[1].set_ylabel('ROC AUC')

axes[1].xaxis.set_major_formatter(

FuncFormatter(lambda x, _: '{:,.0f}'.format(x)))

for i in [0, 1]:

axes[i].tick_params(axis='both', which='major', labelsize=10)

axes[i].tick_params(axis='both', which='minor', labelsize=8)

axes[i].set_xlim(xmin, xmax)

fig.suptitle('Learning Curves', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9)

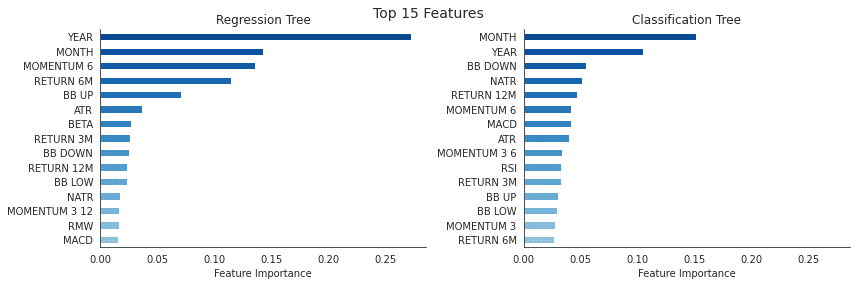

特徴量の重要度

top_n = 15

labels = X.columns.str.replace('_', ' ').str.upper()

fi_clf = (pd.Series(gridsearch_clf.best_estimator_.feature_importances_,

index=labels).sort_values(ascending=False).iloc[:top_n])

fi_reg = (pd.Series(gridsearch_reg.best_estimator_.feature_importances_,

index=labels).sort_values(ascending=False).iloc[:top_n])fig, axes= plt.subplots(ncols=2, figsize=(12,4), sharex=True)

color = cm.Blues(np.linspace(.4,.9, top_n))

fi_clf.sort_values().plot.barh(ax=axes[1], title='Classification Tree', color=color)

fi_reg.sort_values().plot.barh(ax=axes[0], title='Regression Tree', color=color)

axes[0].set_xlabel('Feature Importance')

axes[1].set_xlabel('Feature Importance')

fig.suptitle(f'Top {top_n} Features', fontsize=14)

sns.despine()

fig.tight_layout()

fig.subplots_adjust(top=.9);

この記事が気に入ったらサポートをしてみませんか?