China Reopening in 2023 – What’s Changed in the Economy, Policy, and Diplomacy?, China Briefing, June 27, 2023.

Written by Arendse Huld

China’s recovery after almost three years of stringent COVID-19 restrictions has proven successful but not without its challenges. Recovery has been steady across a range of sectors, while uneven growth has spurred the government to consider policy measures to keep the country on track to reach its 2023 growth target. In this article, we discuss how China’s reopening in 2023 has brought about changes to the economy, policy, and international diplomacy with key partners around the world.

Since emerging from the COVID-19 pandemic, China has embarked on a steady path toward economic recovery. With the lifting of restrictions in late 2022, the country has achieved a rebound in economic activity across a variety of sectors, as well as a near-complete recovery in domestic tourism and a modest increase in international travel.

At the same time, uneven growth across the first five months of 2023 has led the government to roll out and contemplate various measures to support businesses and boost consumption, while tweaking fiscal policy to control market liquidity.

The return of international travel has also enabled new milestones in the country’s foreign relations, with a busy diplomatic calendar seeing scores of new agreements signed to facilitate international business and trade.

In this article, we look at how the country has developed since the lifting of COVID-19 restrictions, from economic recovery to developments in domestic policy and international diplomacy.

Economic recovery after China’s reopening in 2023

China’s economy has been on a trajectory of steady but uneven recovery since the lifting of COVID-19 restrictions. GDP grew by 4.5 percent in the first quarter of 2023, a robust figure that exceeded the 2022 annual GDP growth rate of 3 percent, but was lower than the target of “around 5 percent” set for 2023 in the Government Work Report.

Various economic indicators have shown a steady increase since the end of 2022, including manufacturing, services, and consumption.

Recovery of consumption and services

Services have experienced one of the fastest recoveries of any sector since the end of 2022, in large part because it was one of the industries worst impacted by COVID-19 restrictions. On a year-on-year basis, the sale of consumer goods went from a 1.8 percent contraction in December 2022 to a 5.5 percent expansion in the first two months of 2023, before peaking at 13.5 percent growth in April. Growth in retail sales decelerated slightly in May in a trend seen across multiple economic sectors.

The high April and May figures are in part due to the low base effect, as consumption and services figures were very low in the same period in 2022 due to COVID-19 restrictions. Although there has undoubtedly been a rebound in consumption from 2022, overall, domestic demand has been relatively weak, as shown by the low levels of imports and low inflation. Consumer price index (CPI) in May rose by just 0.2 percent year-on-year, missing forecasts by 0.1 percentage points. Boosting demand has therefore become one of the government’s key goals to spur economic growth.

Rebound in travel

During the 2023 Labor Day Holiday, which took place from April 29 to May 3, the number of domestic trips and the revenue from the domestic tourism industry both exceeded 2019 figures.

Domestic flights have also returned to full capacity. However, flight ticket prices were significantly higher than before the pandemic, increasing by 39 percent from 2019 to an average of RMB 1,211 (US$167) for a one-way domestic flight ticket during the Labor Day Holiday.

China’s Dragon Boat Festival holiday, which in 2023 fell from June 22 to June 24, has shown similarly high levels of travel. There were a total of 106 million domestic trips over the course of the three days, a 32.2 percent year-on-year increase and equivalent to 112.8 percent of 2019 levels. Tourism revenue reached RMB 37.3 billion (US$5.2 billion), up 44.5 percent year-on-year and equivalent to 94.9 percent of 2019 levels. Outbound travel has also increased significantly but remains below pre-pandemic levels. Data from the Civil Aviation Administration of China (CAAC) shows that, by the end of May 2023, 9.98 billion ton-kilometers of international flights had been completed since the beginning of the year. This is up 12.1 percent from the same period in 2022, but still only accounts for 53.9 percent of the distance covered over the same period in 2019.

In addition, although the number of international flight routes has gradually risen, they still haven’t returned to pre-pandemic levels, partly explaining the sluggish recovery of outbound travel. For instance, less than 6 percent of flights between the US and China that existed prior to the pandemic had resumed by the end of May. The low number of flights available is keeping the cost of tickets high, further slowing the recovery of travel and personnel exchange.

The US and China have recently agreed to work on increasing the number of flight routes, which are currently limited to just 12 round trips per week for each country’s airlines.

Manufacturing and industrial output

The industrial output of companies above a designated size (those with a main business income of over RMB 20 million (approx. US$2.9 million), a key indicator of the country’s manufacturing industry, has increased steadily since the beginning of the year. In the first quarter it was up 3 percent year-on-year in the first quarter, 0.3 percentage points higher than that in the fourth quarter of 2022. In March, the value-add of these industrial enterprises was up 3.9 percent year-on-year, 1.5 percentage points higher than that in the first two months, but slightly lower than Reuter’s forecast of 4 percent.

Industrial output continued to accelerate in April, growing 5.6 percent year-on-year, but slowed to 3.5 percent year-on-year in May.

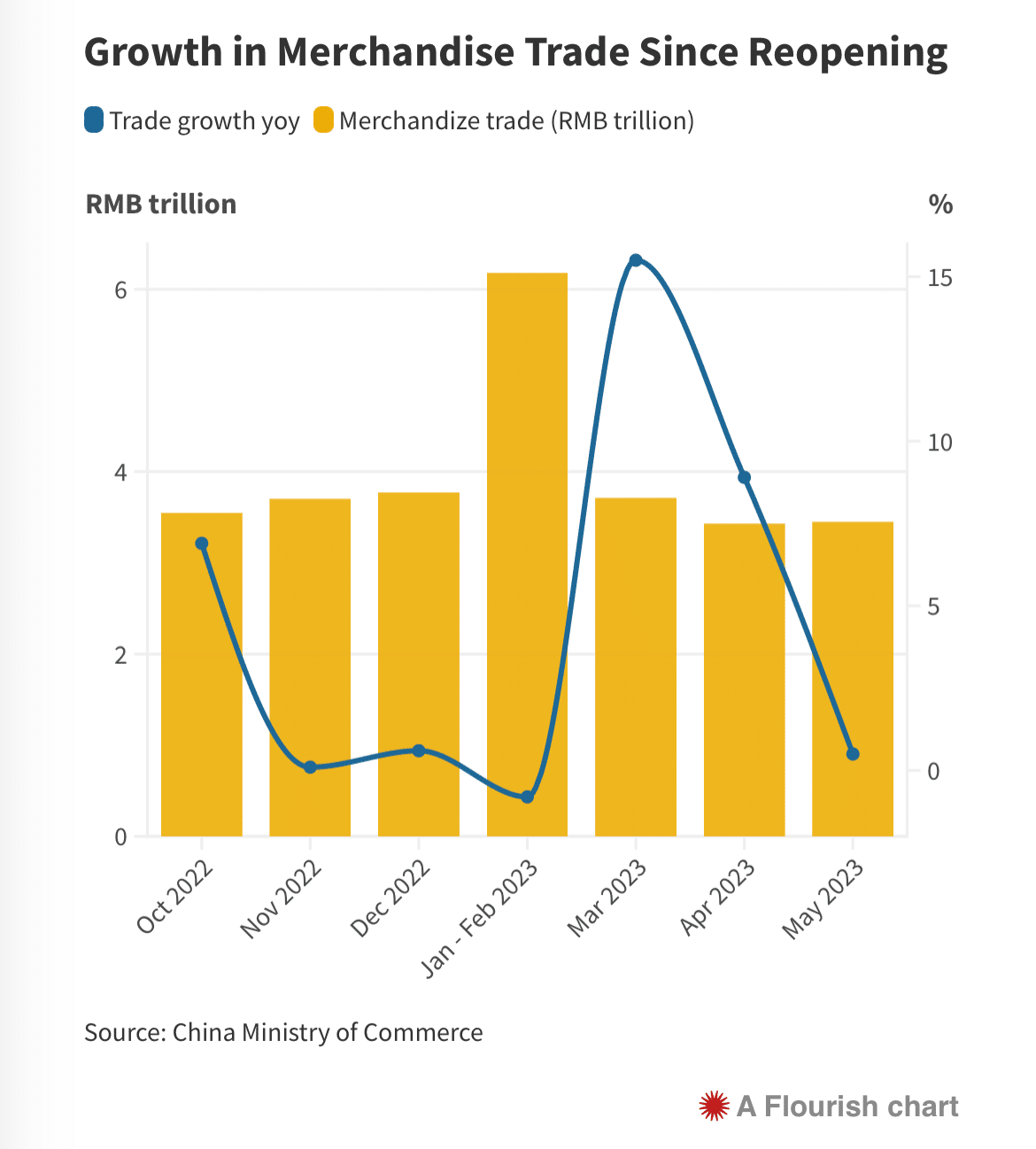

Trade and foreign investment

International trade has remained relatively low since late 2022, with spikes in March and April. In March, the total value of imports and exports increased by 15.5 percent year-on-year, among which exports grew 23.4 percent and imports grew 6.1 percent. This growth rate slowed to 8.9 percent in April and slid further to just 0.5 percent year-on-year in May.

Exports, a key contributor to China’s economic growth, have been particularly impacted by high inflation and an economic recession in key overseas markets, such as the EU and North America. As overseas consumers tighten their belts, they are spending less on Chinese goods. Import volume, meanwhile, has remained consistently low due to weak domestic demand.

Meanwhile, China absorbed RMB 574.8 billion (approx. US$80.3 billion) in the actual use of foreign capital between January and May 2023, according to data from the Ministry of Commerce (MOFCOM). This is a year-on-year increase of 0.1 percent. In dollar terms, the actual use of foreign capital decreased by 5.6 percent to reach US$84.35 billion over this period.

Despite the slow overall growth in FDI, 18,532 foreign-invested enterprises (FIEs) were established across China between January and May, up 38.3 from the same period last year.

Policy developments

Policies to support business and attract foreign investment

In light of the uneven economic recovery, the Chinese government has rolled out policies to support businesses and encourage foreign investment.

At the end of March, the State Council decided to extend several preferential tax policies aimed at supporting small and low-profit companies and key industries. The preferential policies, which include tax deductions for R&D expenses and reduced income tax for small low-profit enterprises and sole proprietors, are expected to reduce the annual tax and fee burden on eligible companies by more than RMB 480 billion (approx. US$69.8 billion).

Provincial and municipal governments have also released plans to support businesses. For instance, Shanghai has released several new measures aimed at attracting FDI, improving the city’s business environment, and supporting private businesses, in an effort to boost business confidence in one of the country’s main economic centers.

Policies to stimulate economic growth

In order to boost economic growth and keep it on target to hit the “around 5 percent” GDP growth, the government has indicated that it will roll out a stimulus package similar to what was seen in 2020.

In a recurring State Council meeting on June 16, presided over by Premier Li Qiang, the State Council addressed issues impeding economic recovery, including an increasingly complex external environment and slowing global trade and investment.

In response to these obstacles, the State Council called for “more forceful measures […] to enhance the momentum of development, optimize the economic structure, and promote the continuous recovery of the economy.” The readout of the meeting stated that the State Council has researched a series of policy measures covering the following areas:

Increasing the intensity of macro-policy regulation;

Focusing on expanding effective demand;

Strengthening and optimizing the real economy; and

Preventing and defusing risks in key areas.

The meeting called for support policies to be introduced “as soon as possible”. According to sources cited by the Wall Street Journal, the government will also seek to boost infrastructure investment, a common tool for stimulating growth, by issuing RMB 1 trillion (approx. US$139.8 billion) worth of special purpose bonds (SPBs).

Monetary and fiscal policy

China has generally adopted a cautious fiscal and monetary policyeven in the face of significant economic turmoil, such as that seen in 2020 and 2022. By using a “prudent” monetary policy throughout the pandemic, the government has previously said it has avoided high inflation and maintained a stable RMB exchange rate.

The government and central bank have maintained this cautious approach to the economy in 2023. In January, the Ministry of Finance (MOF) stated that China would moderately expand fiscal spending in 2023, which will focus on boosting consumption, bolstering food security, and supporting technological development.

On June 15, in order to inject more liquidity into the markets, the People’s Bank of China (PBOC) cut the borrowing rate on the medium-term lending facility (MLF) on RMB 237 billion (approx. US$33.1 billion) worth of loans by 10 basis points, from 2.75 percent to 2.65 percent. The week prior, several of China’s state-owned commercial banks also lowered interest rates on RMB deposits, which could help to reduce lending costs.

On June 19, the PBOC also cut the one-year loan prime rate (LPR) from 3.65 to 3.55 percent and the five-year LPR from 4.3 to 4.2 percent, to lower borrowing costs and boost consumption.

Diplomatic developments

China’s reopening in 2023 and the resumption of international travel have enabled face-to-face diplomatic meetings to take place once again. This has led to a busy diplomatic schedule for the Chinese government in the past few months, with President Xi Jinping hosting several country leaders and making multiple state visits to other countries.

The resumption of in-person diplomacy has been a boon for China, which has successfully deepened trade and investment ties with major countries around the world. For instance, a visit by Brazilian President Luiz Inácio Lula da Silva led to the signing of 15 bilateral agreements estimated to be worth around US$10 billion, which include agreements to facilitate the use of the RMB for trade transactions. In March, China also successfully established diplomatic ties with Honduras, while in April, Argentina announced that it would use RMB to pay for Chinese imports rather than the US dollar in another major step for the internationalization of China’s currency.

On the other side of the globe, China and Australia also resolved a dispute on barley imports, which had halted Australian barley exports to China since 2018.

Deepening relations with the Middle East

China’s relations with countries in the Middle East, and Gulf countries in particular, have continued to deepen in the months since reopening. In December 2022, President Xi Jinping made his first state visit to Saudi Arabia in six years, which resulted in the signing of a “comprehensive strategic partnership agreement” as well as 34 investment agreements covering “several sectors in the fields of green energy, green hydrogen, photovoltaic energy, information technology, cloud services, transportation, logistics, medical industries, housing and construction factories”.

China also notably took center stage in brokering a deal between Saudi Arabia and Iran to restore diplomatic relations between the two powers, which had been broken off since 2016.

A “thaw” in US-China relations

China-US relations have been on rocky ground for many years. While reopening has meant that more high-profile in-person meetings have been possible, in practice, efforts to improve bilateral dialogue have been stymied by various unforeseen events.

President Xi and President Biden held their first face-to-face meeting as leaders in November 2022 in the run-up to the G20 Summit in Bali, Indonesia. In the meeting, the two leaders called for increasing cooperation and communication on major issues “such as climate change, global macroeconomic stability including debt relief, health security, and global food security”.

One outcome of the meeting was also a plan for the US Secretary of State Antony Blinken to visit China in person in early 2023. Originally planned for February, the visit was postponed due to the diplomatic fall-out of the so-called “spy balloon” incident, in which the US accused China of flying a spy balloon across the US in what became a major national news story in the country.

Despite worsening bilateral relations, the two sides have increased the frequency of bilateral dialogue in recent months, with a series of high-level meetings taking place in an effort to defuse tensions. In May, Minister of the Chinese Ministry of Commerce (MOFCOM) Wang Wentao met his US counterpart, the Secretary of Commerce Gina Raimondo at the sidelines of the APEC Trade Ministers’ Meeting in Washington D.C. A few weeks later, Senior US State Department official Daniel Kritenbrink and White House National Security Council’s senior director for China affairs Sarah Beran met with Director-General of the Department of North American and Oceanian Affairs of China’s Ministry of Foreign Affairs Yang Tao and Vice Minister of Foreign Affairs Ma Zhaoxu in Beijing.

Finally, on June 18 and 19, Secretary of State Antony Blinken traveled to Beijing for his rescheduled trip, during which he met with President Xi, Premier Li Qiang, and top Chinese diplomat Wang Yi. The meetings have been hailed as a positive sign of a “thaw” in the relationship and marks an incremental step toward more stable ties. However, progress henceforth will hinge upon the two sides’ ability to handle unforeseen events that could once again derail the relationship.

Rocky China-EU relations

The strength of EU-China relationshas been tested in recent months, with long-standing disputes surrounding market access and technology regulations being exacerbated by an increasingly polarized global political environment. China and the EU have found themselves on opposing sides of the Russia-Ukraine conflict by default, while the EU is under increasing pressure to implement the US’ export controls on chip technology, among other sanctions.

Despite efforts by China to curb the US’ influence, some EU countries have responded to US moves against China. In March, the Netherlands decided to restrict chip technology exports to China, a direct response to the US’ export ban on semiconductor technology.

This hardening attitude is reflected in calls by the President of the European Commission Ursula von der Leyen for Europe to adopt a “de-risking” strategy toward China. On June 20, the European Commission released a strategy to “enhance economic security”, which, although it did not mention China, called for “minimizing risks arising from certain economic flows in the context of increased geopolitical tensions and accelerated technological shifts”.

China has criticized this shift to “de-risking” and rejected the notion that this strategy is different from decoupling. During a recent visit by Chinese Premier Li Qiang to Germany, he warned that “the biggest risk is non-cooperation and the biggest hidden security threat is non-development”.

However, mixed messaging from different European leaders suggests that attitudes toward cooperation with China in the bloc are not uniform. After a visit to China in early April, French President Emmanuel Macron struck a much more balanced tone, calling for Europe to forge its own path in developing relations with China. The visit also resulted in the signing of 18 cooperation agreements between Chinese and French companies.

Earlier, in March 2023, Spanish President Pedro Sánchez also embarked on a state visit to China, in which he reiterated Spain’s stance toward the Russia-Ukraine conflict but also reached an agreement to increase Spanish agricultural exports to China.

China’s recovery going into H2 2023

China’s uneven but steady recovery is expected to continue over the course of the next few months. Despite challenges, most analysts continue to forecast China’s GDP growth for 2023 to be above the “around 5 percent” target. As of June, JPMorgan’s full-year forecast is set at 5.5 percent, while UBS predicts 5.2 percent growth.

The second half of 2023 will doubtlessly come with a series of challenges, whether economic or diplomatic, which will have considerable implications for China’s ongoing economic recovery and business development. Many of these issues are likely to be addressed by corresponding government policies and supportive measures.

We will continue to monitor how China’s economy and position on the world stage develops during the year with timely business analysis and advisory. For updates on China’s economic and business developments after the lifting of COVID-19 restrictions, see our China Reopening Tracker: Latest Developments and Business Advisory.

We also monitor the ongoing developments related to the relationship between China and the US in our Timeline on US-China Relations in the Biden Era.